Point-of-Care Diagnostics Market Size, Share & Forecast 2026–2034

16-May-2026 | Zion Market Research

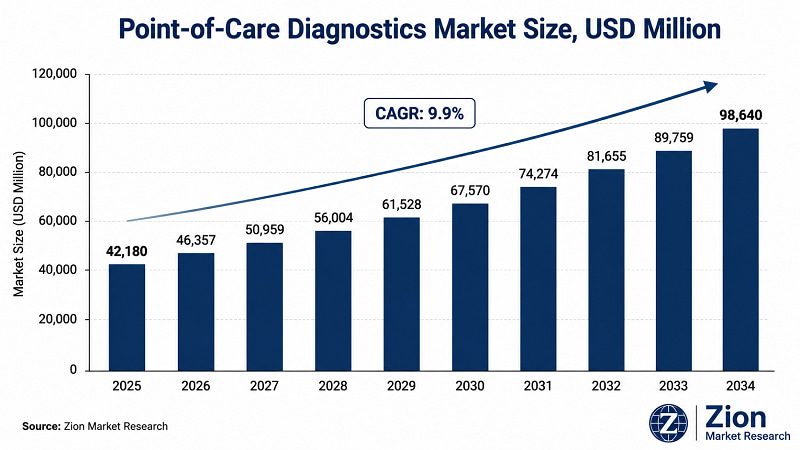

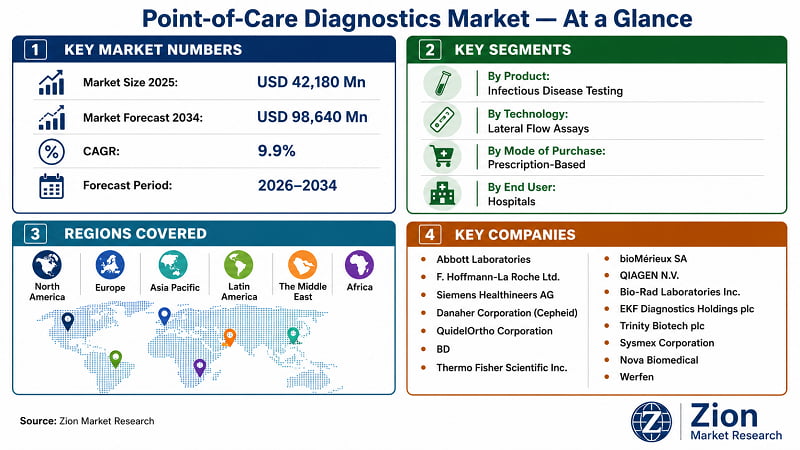

The global Point-of-Care (POC) Diagnostics market was valued at USD 42,180 Mn in 2025. It's forecast to reach USD 98,640 Mn by 2034, registering a 9.9% CAGR over 2026–2034. North America leads by revenue share; Asia Pacific registers the fastest growth. Infectious disease testing and glucose monitoring dominate product demand. According to Zion Market Research, decentralised care adoption and AI-enabled platforms are the primary growth catalysts.

Key Insights Snapshot

|

Attribute |

Detail |

|

Report Title |

Global Point-of-Care Diagnostics Market — Analysis & Forecast, 2026–2034 |

|

Base Year Market Size |

USD 42,180 Mn (2025) |

|

Forecast Market Size |

USD 98,640 Mn (2034) |

|

CAGR |

9.9% (2026–2034) |

|

Forecast Period |

2026–2034 |

|

Dominant Region |

North America (~42% revenue share, 2025) |

|

Fastest-Growing Region |

Asia Pacific (~10.7% CAGR through 2034) |

|

Dominant Segment (Product) |

Infectious Disease Testing (~30–35% share) |

|

Dominant Application |

Decentralised Rapid Testing at Primary Care & Emergency Settings |

|

Report Format |

|

|

Publisher |

Zion Market Research |

What Is the Point-of-Care Diagnostics Market?

- Point-of-Care Diagnostics refers to a broad category of in vitro diagnostic tests and devices that generate clinical results at or near the patient's location — eliminating specimen transport delays and centralised laboratory queues.

- The sector spans glucose monitoring kits, lateral flow immunoassays, molecular PCR platforms, cardiac biomarker panels, coagulation monitors, and an expanding menu of pregnancy, fertility, and drug-of-abuse tests.

- What makes 2025 a structural inflection point is the convergence of three forces that haven't aligned before: widespread CLIA-waived molecular clearances (eight new panels between 2024 and 2025 in the U.S. alone), cloud-connected device management enabling remote quality control across distributed networks, and an accelerating chronic disease burden — 537 million adults globally living with diabetes in 2024, with the International Diabetes Federation projecting 643 million by 2030.

- According to Zion Market Research, the global POC diagnostics market will grow from USD 42,180 Mn in 2025 to USD 98,640 Mn by 2034. The business case is no longer about testing convenience — it's about system-level cost reduction, antimicrobial stewardship, and diagnostic equity.

What Healthcare Decision-Maker Leaders Need to Know About the Point-of-Care Diagnostics Market

- Hospital CIOs & IT Procurement Heads:

POC diagnostics platforms now require full EHR integration and remote quality-control capabilities. Vendors without robust digital connectivity face procurement exclusion. A 9.9% CAGR market through 2034 means capital-allocation decisions made this quarter will determine whether your institution leads or chases adoption. Platforms like Abbott's i-STAT and Roche's cobas Liat that offer cloud-connected, CLIA-waived molecular testing are setting the procurement baseline — alternatives not meeting this standard will be deprioritised.

- Pharma R&D Heads:

The POC diagnostics sector is the fastest-emerging companion diagnostic deployment channel. Molecular assay platforms with multiplex capability are shortening clinical trial site qualification timelines. With the global market scaling from USD 42,180 Mn to USD 98,640 Mn by 2034, companion diagnostic co-development windows are narrowing. Regulatory agencies including the FDA have granted CLIA-waived status to eight molecular respiratory panels between 2024 and 2025 — a regulatory tailwind that compresses time-to-market for novel assay-device combinations.

- Healthcare Investors & PE Firms:

The 9.9% CAGR positions POC diagnostics as one of healthcare's highest-conviction growth categories. North America commands ~42% revenue share at a high per-test average selling price; Asia Pacific is the volume-expansion frontier at an estimated 10.7% CAGR. Consolidation is accelerating — QuidelOrtho's 2025 acquisition of LEX Diagnostics for its ultra-fast molecular platform signals that high-margin molecular POC is the M&A priority category. Investors who missed the COVID-19 wave should note the infrastructure now being built for endemic respiratory, cardiometabolic, and STI testing at scale.

- Regulatory Affairs Directors:

The EU's IVDR deadline of May 2025 removed approximately 30% of legacy POC devices from European markets due to manufacturers' inability to secure notified-body audits. This supply gap is an immediate commercial opportunity for IVDR-compliant platforms. In parallel, the FDA issued Class I recalls affecting over 7 million glucose meters in 2024, raising the bar for clinical accuracy audits. Teams should model regulatory-driven category fragmentation as a demand-creation event, not a market headwind.

- Managed Care Executives:

POC diagnostics directly compress hospital length-of-stay and antibiotic stewardship costs. The UK's National Health Service deployed Roche cobas Liat units across 200 general practices specifically to reduce inappropriate antibiotic prescribing — a model that managed care networks can replicate to drive pharmacy spend reduction. CMS reimburses CLIA-waived molecular assays at USD 45–75 per panel; quantifying the downstream cost avoidance from faster treatment decisions is the business case for network-wide POC formulary adoption.

What Is Driving the Point-of-Care Diagnostics Market?

- Rising Chronic & Infectious Disease Burden:

537 million adults globally lived with diabetes in 2024 — a figure the IDF projects to reach 643 million by 2030. Parallel infectious disease pressures, including dengue outbreaks across Southeast Asia and sustained respiratory pathogen activity, have generated sustained demand for rapid diagnostic platforms that deliver results at the point of treatment rather than 24–72 hours later from centralised labs. Abbott deployed its ID NOW molecular platform — delivering COVID-19 results in 13 minutes — across decentralised physician office and urgent care settings in the U.S., demonstrating the commercial viability of near-patient molecular testing at scale.

- Regulatory Acceleration of CLIA-Waived Molecular Testing:

The FDA's expedited 510(k) pathway cleared 47 new POC devices in 2024 — 22% more than the prior year — and granted CLIA-waived status to eight molecular respiratory panels between 2024 and 2025. CMS reimburses CLIA-waived molecular assays at USD 45–75 per panel, creating a direct economic incentive for practices to upgrade from antigen-based lateral flow tests to higher-sensitivity PCR-class platforms. Cepheid shipped 2.3 million Xpert Xpress units in Q3 2024 alone — a 35% year-on-year surge that illustrates how the regulatory tailwind converts directly into volume demand.

- Decentralisation of Healthcare Delivery:

Health system economics are shifting care from inpatient settings to ambulatory, home, and community-based environments. The U.S. government has allocated over USD 2 billion through the NIH and BARDA to support diagnostic innovation, with a specific emphasis on decentralised settings — outpatient clinics, nursing homes, and homes. Siemens Healthineers expanded its U.S. operations in May 2025 with a USD 150 million investment to strengthen manufacturing, supply-chain resilience, and customer support — a direct response to accelerating demand-side dynamics from health system procurement teams.

- Key Takeaway:

"Our intended acquisition of LEX Diagnostics will strengthen and accelerate our presence in point-of-care molecular diagnostics — one of the largest and fastest-growing segments in the diagnostics industry."

— Brian J. Blaser, President and Chief Executive Officer, QuidelOrtho Corporation

(Source: QuidelOrtho Press Release, June 2025)

"In 2025, we transitioned from COVID-driven volatility to a more durable, diversified diagnostics business. Our Labs, Immunohematology and Cardiac businesses delivered consistent growth, while cost-savings initiatives drove meaningful margin expansion."

— Brian J. Blaser, President and CEO, QuidelOrtho Corporation

(Source: QuidelOrtho Full-Year 2025 Earnings Release, February 2026)

What Is Restraining the Point-of-Care Diagnostics Market?

- Regulatory Complexity & Device Recall Risk:

The FDA issued Class I recalls for 3.7 million TRUEresult and TRUEtrack glucose meters in May 2024 following software errors producing falsely elevated readings. Abbott followed with a voluntary recall of 3.6 million FreeStyle Libre 2 readers in October 2024 due to battery overheating risks. Such events erode clinician confidence and prompt hospital procurement committees to demand third-party accuracy audits before adopting new platforms — extending sales cycles and increasing compliance costs for manufacturers.

- Reimbursement Constraints & Payer Policies:

Private insurers, including Anthem, introduced prior authorisation rules that limit respiratory pathogen panels to high-risk patients, restricting volume in outpatient settings. In Europe, the IVDR deadline of May 2025 forced approximately 30% of legacy POC devices off the market, creating interim supply disruption for healthcare providers dependent on those platforms.

- Supply-Chain Cost Inflation & Tariff Pressure:

Certain diagnostic reagents and lab supplies are now subject to U.S. import duties as high as 25% or more, depending on classification and country of origin, raising landed costs for manufacturers sourcing internationally. Geopolitical instability has contributed to a 2.9% annual rise in supply-chain costs. These pressures raise per-test cost structures and create margin pressure across the distribution chain.

Despite these challenges, the market is expected to grow from USD 42,180 Mn in 2025 to USD 98,640 Mn by 2034.

What Industry Leaders Are Saying About the Point-of-Care Diagnostics Market

"Accurate and timely diagnostic insights are more important than ever. Those insights guide treatment decisions, support faster care for patients, and help healthcare systems operate more efficiently."

— Brian J. Blaser, President and CEO, QuidelOrtho Corporation

(Source: QuidelOrtho 2025 Annual Report Letter to Stockholders)

"The market now rewards vendors that can prove clinical and operational impact — reduced hospital stays, faster therapeutic decisions, or antimicrobial stewardship — rather than mere analytical accuracy. Connectivity has become a critical differentiator; health systems increasingly demand EHR integration, remote quality control, and secure data interoperability."

— Industry Analyst Commentary, Point-of-Care Diagnostics Market Strategic Assessment

(Source: Zion Market Research, Point-of-Care Diagnostics Market Analysis, 2025)

Which Region Leads the Point-of-Care Diagnostics Market?

- North America commands an estimated 42% of global POC diagnostics revenue in 2025, underpinned by the U.S. healthcare system's advanced reimbursement framework, high disease prevalence across chronic and infectious categories, and a concentrated base of technology manufacturers driving platform innovation. The U.S. FDA's expedited 510(k) pathway cleared 47 new POC devices in 2024 — a 22% year-on-year increase — and granted CLIA-waived status to eight molecular respiratory panels between 2024 and 2025, directly stimulating demand at physician offices. Canada and Mexico follow, with Canada showing growing adoption of digital-connected POC devices in emergency department settings.

- Asia Pacific is the fastest-growing region, projected to register approximately 10.7% CAGR through 2034. China's National Medical Products Administration (NMPA) cleared Roche's cobas Liat system in 2024, unlocking access to 36,000 township health centres serving 600 million rural residents — a single regulatory event with transformative TAM expansion implications. India's National Health Mission distributed 15 million Abbott malaria rapid tests in 2025, covering districts where laboratory microscopy is unavailable in 40% of primary health centres. Japan, South Korea, and Australia are extending coverage to continuous glucose monitoring (CGM) and AI-enabled diagnostic systems.

- Europe navigates the EU In Vitro Diagnostic Regulation (IVDR), which removed approximately 30% of legacy POC devices from European markets by May 2025 — creating procurement demand for IVDR-compliant replacements. Germany has expanded reimbursement for patient-managed INR testing; the UK's National Health Service has deployed Roche cobas Liat units in 200 general practices to curb inappropriate antibiotic prescribing. Latin America is led by Brazil, which is expanding diagnostic network density through public health infrastructure programmes. The Middle East is investing in POC platforms across GCC hospital networks, particularly in Saudi Arabia and the UAE. Africa is an emerging frontier, with South Africa, Egypt, and Nigeria as the primary adoption centres driven by infectious disease surveillance mandates.

Report Segmentation & Scope

|

Zion Market Research | Market & Reports — Report Segmentation & Scope |

|

|

Scope Included in the Study |

|

|

By Product |

Glucose Testing • Infectious Disease Testing • Cardiac Markers • Coagulation Testing • HbA1c Testing • Pregnancy & Fertility Testing • Drug-of-Abuse Testing • Others |

|

By Technology |

Lateral Flow Assays • Molecular Diagnostics • Immunoassay Analyzers • Biochemistry |

|

By Mode of Purchase |

Prescription-Based Testing Products • Over-the-Counter (OTC) Testing Products |

|

By End User |

Hospitals • Clinics • Home Settings • Diagnostic Centres • Ambulatory Care Centres |

|

Regional Analysis |

|

|

North America |

The U.S., Canada, Mexico |

|

Europe |

Germany, France, U.K., Italy, Spain, Russia, BENELUX, Sweden, Denmark, Poland, Austria, Rest of Europe |

|

Asia Pacific |

China, Japan, India, South Korea, Australia, Thailand, Indonesia, Vietnam, Malaysia, Philippines, Taiwan, Rest of Asia Pacific |

|

Latin America |

Brazil, Argentina, Colombia, Chile, Peru, Rest of Latin America |

|

The Middle East |

GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman), Israel, Turkey, Iran, Rest of Middle East |

|

Africa |

South Africa, Egypt, Nigeria, Algeria, Morocco, Rest of Africa |

|

Note: The scope can be further tailored as per your specific requirement. Contact sales@zionmarketresearch.com |

|

**Source: Zion Market Research | Global Point-of-Care (POC) Diagnostic Market Report.

Who Are the Leading Companies in the Point-of-Care Diagnostics Market?

- Key players operating in the Global Point-of-Care Diagnostics market include Abbott Laboratories (USA), F. Hoffmann-La Roche Ltd. (Switzerland), Siemens Healthineers AG (Germany), Danaher Corporation / Cepheid (USA), QuidelOrtho Corporation (USA), BD — Becton, Dickinson and Company (USA), Thermo Fisher Scientific Inc. (USA), bioMérieux SA (France), QIAGEN N.V. (Netherlands), Bio-Rad Laboratories Inc. (USA), EKF Diagnostics Holdings plc (UK), Trinity Biotech plc (Ireland), Sysmex Corporation (Japan), Nova Biomedical (USA), and Werfen (USA), among others.

- The competitive landscape is semi-consolidated, with the top five players — Abbott, Roche, Siemens Healthineers, Danaher/Cepheid, and QuidelOrtho — holding a combined majority of global revenue through broad product portfolios and extensive distribution networks. M&A activity is accelerating, with QuidelOrtho's 2025 acquisition of LEX Diagnostics for its ultra-fast molecular platform signalling continued consolidation around high-margin molecular POC segments.

What Recent Developments Are Shaping the Point-of-Care Diagnostics Market?

- Jan 2025 — Roche Diagnostics gained U.S. FDA 510(k) clearance and CLIA waiver for its cobas Liat sexually transmitted infection (STI) multiplex assay panels, expanding the molecular POC menu for physician offices and urgent care clinics.

- Jan 2025 — BD (Becton, Dickinson and Company) announced the global expansion of its BD Veritor Plus platform for rapid COVID-19 and flu combo testing across pharmacies and outpatient settings.

- Jun 2025 — QuidelOrtho Corporation announced its intended acquisition of LEX Diagnostics to accelerate its presence in point-of-care molecular diagnostics — a segment the company described as one of the largest and fastest-growing in the IVD industry.

|

Date |

Company |

Type |

Description |

Market Impact |

|

Jan 2025 |

Roche Diagnostics |

Product Launch / Regulatory |

cobas Liat STI multiplex assay panels received FDA 510(k) clearance and CLIA waiver for point-of-care STI diagnosis including Chlamydia and Gonorrhea |

Expands molecular POC menu into the STI category; enables same-visit diagnosis and treatment across urgent care and sexual health clinics |

|

Jan 2025 |

BD (Becton Dickinson) |

Product Expansion |

Global expansion of BD Veritor Plus platform for rapid COVID-19 and influenza combo testing across pharmacies and outpatient settings |

Strengthens BD's position in the pharmacy and outpatient rapid antigen channel; extends global installed base |

|

May 2025 |

Siemens Healthineers |

Investment |

USD 150 million U.S. operations expansion — new and upgraded manufacturing facilities across multiple states to boost capacity and customer support |

Signals vendor confidence in sustained North America demand; improves supply-chain resilience for hospital system procurement |

|

Jun 2025 |

QuidelOrtho Corporation |

M&A / Strategy |

Announced intended acquisition of LEX Diagnostics for its ultra-fast molecular diagnostics platform to strengthen POC molecular presence |

Accelerates QuidelOrtho's molecular POC positioning; LEX platform offers performance advantages over prior Savanna platform |

|

Oct 2025 |

BARDA / Beckman Coulter |

Research Funding / Investment |

BARDA awarded funding to Beckman Coulter to validate effectiveness of biomarker for MIS-C detection through a large multi-centre clinical trial |

Demonstrates continued U.S. government investment in POC diagnostic infrastructure; validates biomarker-driven POC expansion |

|

Feb 2025 |

Aptitude Medical Systems |

Regulatory |

Metrix COVID/Flu multiplex test received FDA Emergency Use Authorization — first molecular POC test cleared for CLIA-waived and home settings for flu A, flu B, and SARS-CoV-2 differentiation in 20 minutes |

Expands home-based molecular POC market; removes last major barrier between clinical-grade molecular accuracy and consumer self-testing |

About Us:

Zion Market Research is an obligated company. We create futuristic, cutting-edge, informative reports ranging from industry reports, the company reports to country reports. We provide our clients not only with market statistics unveiled by avowed private publishers and public organizations but also with vogue and newest industry reports along with pre-eminent and niche company profiles. Our database of market research reports comprises a wide variety of reports from cardinal industries. Our database is been updated constantly in order to fulfill our clients with prompt and direct online access to our database. Keeping in mind the client’s needs, we have included expert insights on global industries, products, and market trends in this database. Last but not the least, we make it our duty to ensure the success of clients connected to us—after all—if you do well, a little of the light shines on us.

Author:

Mr. Nilesh Patil

Director at Zion Market Research

LinkedIn- www.linkedin.com/in/nilesh-patil-m-s-m-b-a-bba33067