Cluster Packaging Market Size, Share and Forecast Report 2034

Cluster Packaging Market By Type (Single Tier Cluster Packaging and Multiple Tier Cluster Packaging), By Application (Food & Beverages, Personal Care and Cosmetics Industry, Pharmaceuticals & Healthcare, Industrial Goods and Others), By Material (Plastic, Glass and Paperboard), By Distribution Channel (Offline Retail, Online Retail and Direct to Consumer) and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

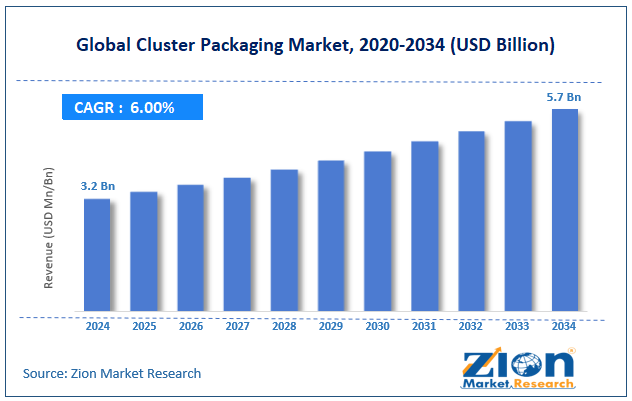

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 3.2 Billion | USD 5.7 Billion | 6.0% | 2024 |

Cluster Packaging Industry Perspective:

What will be the size of the global cluster packaging market during the forecast period?

The global cluster packaging market size was worth around USD 3.2 billion in 2024 and is predicted to grow to around USD 5.7 billion by 2034 with a compound annual growth rate (CAGR) of roughly 6.0% between 2025 and 2034.

Request Free SampleRequest Free Sample

Request Free SampleRequest Free Sample

Key Insights

- As per the analysis shared by our research analyst, the global cluster packaging market is estimated to grow annually at a CAGR of around 6.0% over the forecast period (2025-2034).

- In terms of revenue, the global cluster packaging market size was valued at around USD 3.2 billion in 2024 and is projected to reach USD 5.7 billion by 2034.

- Expansion of retail and e-commerce channels is expected to propel the cluster packaging market over the projected period.

- Based on the type, the multiple tier cluster packaging segment captures the largest market share in 2024.

- Based on the application, the food & beverages segment holds the largest market share over the projected period.

- Based on the material, the paperboard segment holds a prominent revenue share of over 35%.

- Based on the distribution channel, the offline retail segment holds the largest market share over the projected period.

- Based on region, the Asia Pacific captures the largest market share in 2024.

Cluster Packaging Market: Overview

The cluster packaging approach is one of the most popular forms of secondary packaging, in which several items are grouped into a single unit to simplify their transport, storage, packing, and presentation for retail display. Some common applications of the cluster packaging include food and beverage products, personal hygiene products, household consumer goods, and pharmaceuticals, and involve products such as beverages, bottles, yogurt, and consumer goods in multipacks. Paperboard, corrugated board, plastic film, and other similar materials can be used as carriers for products under this form of packaging, with the aim of minimizing the packaging weight/materials required. Cluster packaging offers better shelf visibility, provides convenience for consumers, supports efficient palletization/logistics operations, and reduces packaging costs for manufacturers.

Impact of the USA-Israel War on Iran on the Cluster Packaging Market

The prolonged war between the USA and Israel concerning Iran has adversely affected the cluster packaging market due to supply chain disruptions, high crude oil and petrochemical prices, and higher transport and raw material costs. The fact is that the production of cluster packaging is highly dependent on the availability of paperboard, plastic, adhesive, ink, and aluminum products. Additionally, disturbances in the Strait of Hormuz have disrupted delivery processes, leading to shortages of packaging materials. Finally, the increase in inflation has forced manufacturers to keep packaging costs down.

Cluster Packaging Market: Dynamics

Growth Drivers

Why does the rising demand for sustainable packaging drive the cluster packaging market?

With the rising demand for sustainability in packaging, several growth opportunities will arise in the cluster packaging industry, owing to lower raw material consumption, lower plastic usage, and recyclability compared to traditional secondary packaging. Most existing cluster packaging materials on the market are made of paperboard and fiber, rather than regular plastics or bulky cardboard boxes, thereby helping organizations comply with environmental and sustainability policies. Furthermore, cluster packaging is lightweight, enabling reduced transport costs and lower carbon footprints. There is growing consumer demand for sustainable multipacks of drinks, foods, and other consumer goods.

Restraints

Volatility in raw material prices hinders the growth of the cluster packaging industry

The instability of raw material prices is one of the main inhibitors to the development of the Cluster Packaging Market, as it largely relies on materials such as paperboard, corrugated cardboard, plastic, adhesive, ink, and aluminum. The frequent changes in pulp, petrochemicals, and energy prices add additional costs for packaging producers during manufacturing and shipping, resulting in lower margins and increased pricing pressures throughout the production process. Moreover, due to higher raw-material costs, many firms tend to charge consumers more for their products, thereby preventing certain industries from adopting new technology.

Opportunities

Why does the rising product portfolio expansion by the key players offer a lucrative opportunity for the cluster packaging market?

The rising product portfolio expansion by the key players are expected to florish the cluster packaging market over the projected period. For instance, in November 2025, one of the world's leading manufacturers of packaging solutions for food and beverages, Lamipak, presented its latest product offerings at Gulfood Manufacturing 2025. This event was considered one of the company's most successful in terms of participation. Lamipak launched an innovative product line aimed at increasing sustainability, performance, and customer experience, as well as reinforcing its position in the market as an all-in-one aseptic packaging solution in the Middle East, Africa, and the Indian subcontinent. LamiSleeve emerged as one of the key introductions from the company at the Gulfood Manufacturing 2025 trade fair. Through this launch, Lamipak became the first company to offer a full aseptic beverage carton product line, available in both roll-fed and sleeve packaging.

Challenges

Why does the competition from alternative packaging formats pose a significant challenge to the cluster packaging market?

Competitive pressure from other packaging forms is a major obstacle the cluster packaging sector faces, as the manufacturing industry has access to many other options that are less expensive and highly adaptable, such as flexible packaging, shrink wraps, corrugated packaging, plastic carriers, and stand-up pouches. Some benefits associated with these options include reduced material use, increased strength, ease of modification, and enhanced protection during transit. In some cases, especially for bulkier or odd-shaped items, these other forms of packaging may be stronger and better at protecting against moisture than cluster packaging.

Furthermore, many companies are set up to produce other forms of packaging and thus find it difficult and expensive to adopt cluster packaging.

Cluster Packaging Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Cluster Packaging Market |

| Market Size in 2024 | USD 3.2 Billion |

| Market Forecast in 2034 | USD 5.7 Billion |

| Growth Rate | CAGR of 6.0% |

| Number of Pages | 227 |

| Key Companies Covered | Amcor Limited, International Paper Company, Ball Corporation, Berry Global Group Inc., DS Smith Plc, Owens-Illinois Inc., Mondi Group, Sealed Air Corporation, Smurfit Kappa Group, Sonoco Products Company, Stora Enso Oyj, Tetra Pak International S.A., WestRock Company, Graphic Packaging International LLC, Huhtamaki Oyj, and others. |

| Segments Covered | By Type, By Application, By Material, By Distribution Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Cluster Packaging Market: Segmentation

Type Insights

Why does the multiple tier cluster packaging dominate the cluster packaging market?

The multiple tier cluster packaging segment captures the largest market share in 2024. This growth is attributed to high demand for its use in the packaging of beverages, food, and bulk consumer products. Such a packaging method is engineered to package products in multiple tiers or layers, making packaging more efficient, stable, and easier to arrange on store shelves. Multiple-tier cluster packaging is preferred for beverage containers and other bulky retail products, as it optimizes the use of shipping pallets.

Application Insights

How does the food & beverages segment capture the largest market share in the cluster packaging market?

The food & beverages segment holds the largest market share over the projected period. The driver of segment growth is the widespread adoption of cluster packaging across multipacks of bottled water, soft drinks, alcoholic beverages, dairy products, canned foods, and ready-to-drink beverages. Cluster packaging is widely adopted by beverage producers because it makes packaging easier to handle, increases shelf visibility, reduces packaging material consumption, and facilitates transportation. Rising demand for convenience packaging, bulk purchases, and multipacks of sustainable beverages made from paperboard has resulted in the food & beverages segment dominating the market.

Some prominent beverage companies adopting cluster packaging for their cans and bottled beverages include The Coca-Cola Company, PepsiCo, and Anheuser-Busch InBev. Multipacks of beverages and processed food products sold across supermarkets, hypermarkets, and warehouse retailers have driven the food & beverages segment's high market share in the cluster packaging market.

Material Insights

Does the paperboard segment capture the largest market share in the cluster packaging market?

The paperboard segment holds a prominent revenue share of over 35%. This growth can be attributed to the ever-growing global need for environmentally friendly, lightweight, and recyclable packaging materials. Paperboard-based clustered packaging is commonly used in the food and beverage industry for packaging beverages, canned drinks, dairy products, and other multipacks of consumer goods, as it reduces plastic use without compromising product integrity or packaging aesthetics. Increasing restrictions on single-use plastics, along with growing numbers of environmentally conscious consumers, are driving the adoption of fibers.

Distribution Channel Insights

Why does the offline retail segment capture the largest market share in the cluster packaging market?

The offline retail segment holds the largest market share over the projected period. The rise is attributed to the increase in supermarkets, hypermarkets, warehouse clubs, and convenience stores offering multipacks of products. The adoption of cluster packaging is common in physical retail shops due to its effectiveness in boosting product visibility, making product stocking on shelves easier, improving handling efficiency, and enabling promotion bundling of beverages, foods, domestic goods, and toiletries. Cluster packaging is favored by retailers for mass buying and product display, especially for bottles of beverages, cans of drinks, and ready meals.

Regional Insights

Why does the Asia Pacific lead the cluster packaging market?

The Asia Pacific captures the largest market share in 2024. Due to factors such as urbanization, population growth, rising disposable incomes, and rapid development in food and beverages in countries like China, India, Japan, and South Korea, the Asia-Pacific is experiencing massive growth. Cluster packaging solutions have been prompted by the use of beverages, dairy products, canned foods, and home-care products in the region. In addition, due to the rapid growth in the number of supermarkets, hypermarkets, convenience stores, and e-commerce logistics in the Asia Pacific region, there is a strong need for multi-packing solutions to improve efficiency in handling and transportation.

Besides that, the Asia Pacific region has advantages in manufacturing capacity, low-cost manufacturing, and sustainable packaging solutions. The growing awareness of environmental problems, along with measures taken by various governments to reduce plastic waste, has pushed manufacturers to adopt cluster packaging made from recycled paperboard.

Cluster Packaging Market: Competitive Analysis

The global cluster packaging market is dominated by players like:

- Amcor Limited

- International Paper Company

- Ball Corporation

- Berry Global Group Inc.

- DS Smith Plc

- Owens-Illinois Inc.

- Mondi Group

- Sealed Air Corporation

- Smurfit Kappa Group

- Sonoco Products Company

- Stora Enso Oyj

- Tetra Pak International S.A.

- WestRock Company

- Graphic Packaging International LLC

- Huhtamaki Oyj

The global cluster packaging market is segmented as follows:

By Type

- Single Tier Cluster Packaging

- Multiple Tier Cluster Packaging

By Application

- Food & Beverages

- Personal Care and Cosmetics Industry

- Pharmaceuticals & Healthcare

- Industrial Goods

- Others

By Material

- Plastic

- Glass

- Paperboard

By Distribution Channel

- Offline Retail

- Online Retail

- Direct to Consumer

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- The Middle East & Africa

- Saudi Arabia

- UAE

- Egypt

- Kuwait

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Table Of Content

Methodology

FrequentlyAsked Questions

The cluster packaging approach is one of the most popular forms of secondary packaging, in which several items are grouped into a single unit to simplify their transport, storage, packing, and presentation for retail display.

Key growth drivers for the cluster packaging market include rising demand for sustainable packaging, increasing consumption of multipack food and beverages, growth of organized retail and e-commerce, and the need for cost-efficient, lightweight packaging solutions.

Major challenges restraining the growth of the cluster packaging market include volatility in raw material prices, competition from alternative packaging formats, high machinery investment costs, and recycling limitations for multi-material packaging solutions.

Based on the type, the multiple tier cluster packaging segment is expected to dominate the cluster packaging market growth during the projected period.

Emerging trends and innovations impacting the cluster packaging market include the adoption of recyclable paperboard packaging, lightweight multipack designs, smart automated packaging systems, and sustainable plastic-free cluster packaging solutions.

According to the report, the global cluster packaging market size was worth around USD 3.2 billion in 2024 and is predicted to grow to around USD 5.7 billion by 2034.

The global cluster packaging market is expected to grow at a CAGR of 6.0% during the forecast period.

The global cluster packaging industry growth is expected to be led by the Asia Pacific over the forecast period.

The global cluster packaging market is dominated by players like Amcor Limited, International Paper Company, Ball Corporation, Berry Global Group, Inc., DS Smith Plc, Owens-Illinois, Inc., Mondi Group, Sealed Air Corporation, Smurfit Kappa Group, Sonoco Products Company, Stora Enso Oyj, Tetra Pak International S.A., WestRock Company, Graphic Packaging International, LLC and Huhtamaki Oyj among others.

The market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

HappyClients