Liquid Crystal Display (LCD) Market Size Report, Share, Analysis, Growth, 2030

Liquid Crystal Display (LCD) Market By Application (Small Appliances, Industrial, Automotive, Medical, Consumer Goods, and Others), By Product (LCD Graphic Drivers, LCD Character Drivers, and LCD Segment Drivers), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2023 - 2030

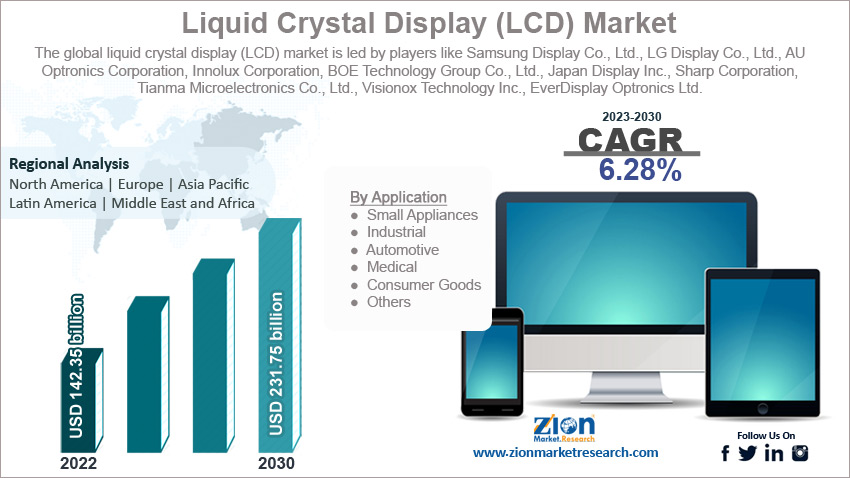

| Market Size in 2022 | Market Forecast in 2030 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 142.36 Billion | USD 231.75 Billion | 6.28% | 2022 |

Liquid Crystal Display (LCD) Industry Prospective:

The global liquid crystal display (LCD) market size was worth around USD 142.36 billion in 2022 and is predicted to grow to around USD 231.75 billion by 2030 with a compound annual growth rate (CAGR) of roughly 6.28% between 2023 and 2030.

The report analyzes the global liquid crystal display (LCD) market drivers, restraints/challenges, and the effect they have on the demands during the projection period. In addition, the report explores emerging opportunities in the liquid crystal display (LCD) industry.

-market-size.png)

Liquid Crystal Display (LCD) Market: Overview

Liquid crystal display (LCD) is a flat-panel display technology that has multiple applications and is used in several modern electronic devices such as televisions, computer monitors, smartphones, and digital watches. LCD devices are popular owing to their lightweight and thin design which makes them suitable for a range of applications. The display is made of a layer of liquid crystals that is placed between two transparent electrodes and two polarizing filters.

The liquid crystals are made of rod-shaped molecules that can align themselves depending on the electric current that they are subjected to. This alignment in turn is responsible for determining the amount of light that passes through them. The industry deals with the economic aspects of designing, manufacturing, marketing, distributing, and after-sales services of LCDs across end-user verticals. During the forecast period, it is expected to grow at a steady rate.

Key Insights:

- As per the analysis shared by our research analyst, the global liquid crystal display (LCD) market is estimated to grow annually at a CAGR of around 6.28% over the forecast period (2023-2030)

- In terms of revenue, the global liquid crystal display (LCD) market size was valued at around USD 142.36 billion in 2022 and is projected to reach USD 231.75 billion, by 2030.

- The liquid crystal display market is projected to grow at a significant rate due to the growing demand in the consumer electronic segment

- Based on application segmentation, the small appliance was predicted to show maximum market share in the year 2022

- Based on product segmentation, LCD character drivers were the leading product in 2022

- On the basis of region, Asia-Pacific was the leading revenue generator in 2022

Liquid Crystal Display (LCD) Market: Growth Drivers

Increasing demand in the consumer electronic segment to propel market growth

The global liquid crystal display (LCD) market is projected to witness high growth owing to the increasing demand in the consumer electronic segment which is one of the fastest-growing sectors. LCDs have become a common choice amongst consumers for a range of products such as televisions, computer monitors, smartphones, laptops, and tablets. Reports have indicated that LCD televisions are the most preferred choice amongst buyers as compared to older display technologies. Furthermore, the industry players have managed to create greater demand in the industry by adding product innovation strategies and providing consumers with an improved experience by integrating more modern systems that align with liquid crystal display technology. The trend is further strengthened by the availability of LCD devices across price ranges and hence cater to a broader range of audience.

Liquid Crystal Display (LCD) Market: Restraints

Increasing competition from alternatives to restricting the market growth

The global liquid crystal display industry is expected to face certain growth restrictions owing to the increasing competition and demand for Organic Light Emitting Diode (OLED) technology since it offers more advantages as compared to LCD. Some of the added benefits include better contrast, wider viewing angles, and faster response times when compared to LCDs. With an increasing rate of well-informed population which is constantly seeking more advanced systems, LCDs may seem to be an outdated technology and hence market players should consistently invest in research and innovation.

Liquid Crystal Display (LCD) Market: Opportunities

Rising investment toward interactive technology to provide growth opportunities

Since the global liquid crystal display market is highly competitive not only within its circle but also in terms of alternate technologies, the industry can survive only by improving its product offering. One such key area of focus lies in developing more interactive displays and touchscreens with better response time. Several companies have directed resources toward exploring the segments of multitouch, gesture recognition, and stylus support which are expected to ensure that consumers can enjoy an immersive experience.

Liquid Crystal Display (LCD) Market: Challenges

High power consumption to challenge market growth

LCDs generally tend to require high-power inputs. This is due to the need for backlighting systems that assist in providing the necessary illumination to the display. This is a significant challenge that can impede global liquid crystal display market growth, especially in regions that do not have access to adequate electricity infrastructure. Furthermore, the economic slowdown in several countries may result in losses over time.

Liquid Crystal Display (LCD) Market: Segmentation

The global liquid crystal display (LCD) market is segmented based on application, product, and region.

Based on application, the global market segments are small appliances, industrial, automotive, medical, consumer goods, and others. The liquid crystal display industry witnessed the highest growth in the small appliances segment and consumer goods. LCD technology is one of the most commonly used tools in the production of devices such as smartphones and tablets along with similar systems including digital watches and cameras. With the increased revenue in the consumer goods sector, the segment is projected to emerge as the largest application of LDC. In the industrial sector, LCDs are employed in control panels, human-machine interfaces (HMIs), industrial automation systems, and equipment displays. They are also integrated with automotive dashboard displays, infotainment systems, instrument clusters, and rear-seat entertainment systems. Typically, consumer goods with LCD technology have a maximum resolution of 1920x1080 pixels.

Based on the product, the global market segments are LCD graphic drives, LCD character drivers, and LCD segment drivers. The highest revenue was generated in the LCD character drivers in 2022. These systems are generally designed for controlling character-based displays which are found in devices such as digital watches, calculators, and some industrial equipment. They consist of a limited set of predefined characters or symbols that are arranged in rows and columns. On the other hand, LCD graphic drivers are used for controlling more complex graphic displays and they can display custom images, icons, and fonts. Their application mainly consists of smartphones, tablets, computer monitors, and graphic user interfaces (GUIs). LCD segment drivers are mostly used in digital clocks, microwave ovens, and automotive dashboard displays. In 2022, India witnessed a 22% year-on-year growth in its smart TV segment.

Recent Developments:

- In November 2022, Detel Mobile and Accessories, one of the world’s most economical feature phone brands as per company claims, announced the launch of a range of the least expensive LCD TVs for the Indian market. The TV set is priced at INR 3,999. The company eyed a revenue of USD 100 crore in the corresponding fiscal year

- In April 2023, HKC Corporation, a China-based manufacturer of LCD screens, announced a collaboration with Japan Display (JDI). The move will allow HKC to use JDI’s latest technology for the production of active-matrix organic light-emitting diode (AMOLED) displays. In 2022, JDI announced the innovation of breakthrough technology. To achieve its goal HKC is expected to billion across its production facilities in China

- In April 2023, Innolux, a leading panel maker, announced its plan to consolidate the production of its outdated LCD fabs

Liquid Crystal Display (LCD) Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Liquid Crystal Display (LCD) Research Report |

| Market Size in 2022 | USD 142.36 Billion |

| Market Forecast in 2030 | USD 231.75 Billion |

| Growth Rate | CAGR of 6.28% |

| Number of Pages | 215 |

| Key Companies Covered | Samsung Display Co., Ltd., LG Display Co., Ltd., AU Optronics Corporation, Innolux Corporation, BOE Technology Group Co., Ltd., Japan Display Inc., Sharp Corporation, Tianma Microelectronics Co., Ltd., Visionox Technology Inc., CSOT (TCL China Star Optoelectronics Technology), EverDisplay Optronics Ltd., Truly International Holdings Limited, HannStar Display Corporation, Chunghwa Picture Tubes Ltd., CPT Technology (Group) Co., Ltd., Himax Technologies, Inc., IVO (InnoVision Optoelectronics) Group, E Ink Holdings Inc., Shenzhen China Star Optoelectronics Technology Co., Ltd., Japan OLED, RiTdisplay Corporation, Sharp NEC Display Solutions, Ltd., Mitsubishi Electric Corporation, Panasonic Corporation, and Toshiba Corporation. |

| Segments Covered | By Application, By Product, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2022 |

| Historical Year | 2017 to 2021 |

| Forecast Year | 2023 - 2030 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Liquid Crystal Display (LCD) Market: Regional Analysis

Asia-Pacific to act as the key regional market

The global liquid crystal display (LCD) market is projected to witness the highest growth in Asia-Pacific and the main reason for high regional growth is the dominant authority of China as the world’s largest supplier of LCD screens to several end-user verticals including some of its competitors in the consumer group segment such as Apple Inc. Other countries like Japan, Taiwan, and South Korea are also leading manufacturers and distributors of LCDs. These countries have managed to create an established manufacturing economy for semiconductors and technologies such as LCD and OLED. Furthermore, companies operating in the region have managed to bring revolutionary technological innovation in terms of display tools and hence have continued to dominate the segment. Moreover, the presence of a larger consumer database in China and India along with other countries acts as a significant source of income in the regional market.

Liquid Crystal Display (LCD) Market: Competitive Analysis

The global liquid crystal display (LCD) market is led by players like:

- Samsung Display Co. Ltd.

- LG Display Co. Ltd.

- AU Optronics Corporation

- Innolux Corporation

- BOE Technology Group Co. Ltd.

- Japan Display Inc.

- Sharp Corporation

- Tianma Microelectronics Co. Ltd.

- Visionox Technology Inc.

- CSOT (TCL China Star Optoelectronics Technology)

- EverDisplay Optronics Ltd.

- Truly International Holdings Limited

- HannStar Display Corporation

- Chunghwa Picture Tubes Ltd.

- CPT Technology (Group) Co. Ltd.

- Himax Technologies Inc.

- IVO (InnoVision Optoelectronics) Group

- E Ink Holdings Inc.

- Shenzhen China Star Optoelectronics Technology Co. Ltd.

- Japan OLED

- RiTdisplay Corporation

- Sharp NEC Display Solutions Ltd.

- Mitsubishi Electric Corporation

- Panasonic Corporation

- Toshiba Corporation.

The global liquid crystal display (LCD) market is segmented as follows:

By Application

- Small Appliances

- Industrial

- Automotive

- Medical

- Consumer Goods

- Others

By Product

- LCD Graphic Drivers

- LCD Character Drivers

- LCD Segment Drivers

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

Liquid crystal display (LCD) is a flat-panel display technology that has multiple applications and is used in several modern electronic devices such as televisions, computer monitors, smartphones, and digital watches.

The global liquid crystal display (LCD) market is projected to witness high growth owing to the increasing demand in the consumer electronic segment which is one of the fastest-growing sectors.

According to study, the global liquid crystal display (LCD) market size was worth around USD 142.36billion in 2022 and is predicted to grow to around USD 231.75 billion by 2030.

The CAGR value of the liquid crystal display (LCD) market is expected to be around 6.28% during 2023-2030.

The global liquid crystal display (LCD) market is projected to witness the highest growth in Asia-Pacific and the main reason for high regional growth is the dominant authority of China as the world’s largest supplier of LCD screens to several end-user verticals including some of its competitors in the consumer group segment such as Apple Inc.

The global liquid crystal display (LCD) market is led by players like Samsung Display Co., Ltd., LG Display Co., Ltd., AU Optronics Corporation, Innolux Corporation, BOE Technology Group Co., Ltd., Japan Display Inc., Sharp Corporation, Tianma Microelectronics Co., Ltd., Visionox Technology Inc., CSOT (TCL China Star Optoelectronics Technology), EverDisplay Optronics Ltd., Truly International Holdings Limited, HannStar Display Corporation, Chunghwa Picture Tubes Ltd., CPT Technology (Group) Co., Ltd., Himax Technologies, Inc., IVO (InnoVision Optoelectronics) Group, E Ink Holdings Inc., Shenzhen China Star Optoelectronics Technology Co., Ltd., Japan OLED, RiTdisplay Corporation, Sharp NEC Display Solutions, Ltd., Mitsubishi Electric Corporation, Panasonic Corporation, and Toshiba Corporation.

Choose License Type

RelatedNews

Zion Market Research

Tel: +1 (302) 444-0166

USA/Canada Toll Free No.+1 (855) 465-4651

3rd Floor,

Mrunal Paradise, Opp Maharaja Hotel,

Pimple Gurav, Pune 411061,

Maharashtra, India

Phone No +91 7768 006 007, +91 7768 006 008

US OFFICE NO +1 (302) 444-0166

US/CAN TOLL FREE +1 (855) 465-4651

Email: sales@zionmarketresearch.com

We have secured system to process your transaction.

Our support available to help you 24 hours a day, five days a week.

Monday - Friday: 9AM - 6PM

Saturday - Sunday: Closed