Global Medical Oxygen Concentrators Market Size, Share, Analysis, Trends, Growth Report, 2030

Global Medical Oxygen Concentrators Market By Product Type (Stationary Oxygen Concentrators, and Portable Oxygen Concentrators), By Technology (Continuous Flow Oxygen Concentrators, and Pulse Flow Oxygen Concentrators), By Application (Home Care, Hospitals, and Ambulatory Surgical Centers (ASCs)), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2023 - 2030

| Market Size in 2022 | Market Forecast in 2030 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 3,552 Million | USD 8,112 Million | 6.2% | 2022 |

Medical Oxygen Concentrators Industry Prospective:

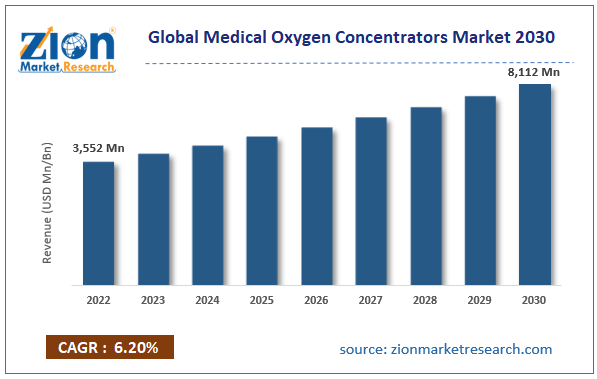

The global medical oxygen concentrator’s market size was worth around USD 3,552 million in 2022 and is predicted to grow to around USD 8,112 million by 2030 with a compound annual growth rate (CAGR) of roughly 6.2% between 2023 and 2030.

Global Medical Oxygen Concentrators Market: Overview

Medical oxygen concentrators play a crucial role in providing concentrated oxygen to individuals with respiratory issues. These devices work by filtering out impurities from room air and delivering a continuous supply of pure oxygen to patients through masks or nasal cannulas. They are widely utilized in both medical facilities and homes, playing a vital role in managing conditions such as COPD. By offering a reliable and consistent source of oxygen, these machines greatly improve the quality of life for those struggling with respiratory ailments. Their ease of use, reliability, and ability to deliver a steady oxygen flow make them an essential tool in the treatment of respiratory illnesses.

Key Insights

- As per the analysis shared by our research analyst, the global medical oxygen concentrators industry is estimated to grow annually at a CAGR of around 6.2% over the forecast period (2023-2030).

- In terms of revenue, the global medical oxygen concentrator’s market size was valued at around USD 3,552 million in 2022 and is projected to reach USD 8,112 million, by 2030.

- The global medical oxygen concentrators market is projected to grow at a significant rate due to the increased frequency of respiratory illnesses, along with an aging population, is boosting demand for dependable respiratory support equipment.

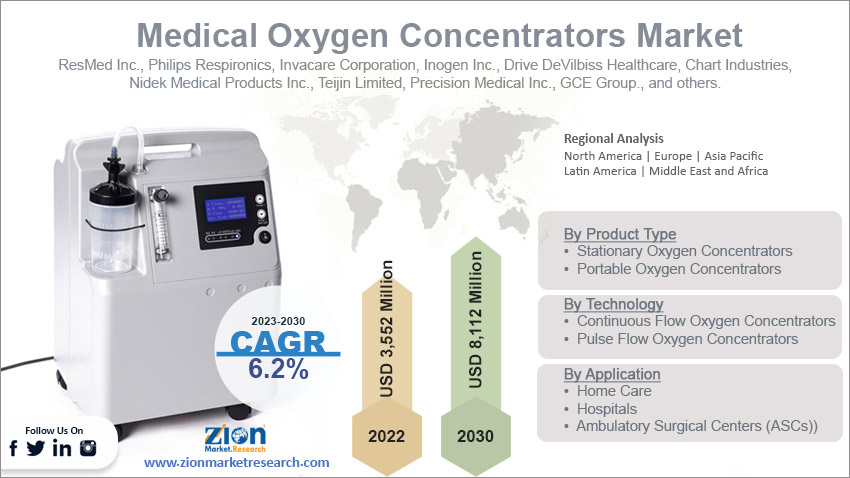

- Based on product type segmentation, stationary oxygen concentrators was predicted to hold maximum market share in the year 2022.

- Based on technology segmentation, continuous flow oxygen concentrators were predicted to hold maximum market share in the year 2022.

- Based on application segmentation, home care was the leading revenue generator in 2022.

- On the basis of region, Asia Pacific was the leading revenue generator in 2022.

Request Free Sample

Request Free Sample

Global Medical Oxygen Concentrators Market: Growth Drivers

Increasing prevalence of respiratory disorders globally, coupled with the rising aging population boosts market growth

As respiratory disorders including chronic obstructive pulmonary disease (COPD), asthma, and pneumonia become more common, there is a greater need for dependable and effective respiratory support equipment. Medical oxygen concentrators, with their capacity to deliver a constant and concentrated supply of oxygen, play an important role in the treatment of several respiratory disorders. The elderly population is especially vulnerable to respiratory disorders, increasing the need for oxygen concentrators as a reliable therapeutic approach. As healthcare professionals and people seek improved and easy respiratory care choices, market demand is increasing. Furthermore, technical improvements and breakthroughs in medical oxygen concentrators help to drive market growth.

Ongoing research and development efforts are aimed at enhancing these devices' efficiency, portability, and user-friendliness. Oxygen concentrators are becoming increasingly appealing to both healthcare professionals and patients due to improved features such as smaller designs, longer battery life, and better monitoring capabilities. The combination of an increasing patient population in need of respiratory assistance and continual developments in device technology sets the worldwide medical oxygen concentrators market for long-term growth.

Global Medical Oxygen Concentrators Market: Restraints

High cost associated with medical oxygen concentrators restrains market growth

The related cost is a significant limitation in the worldwide medical oxygen concentrators market, which can make widespread adoption difficult, particularly in nations with low healthcare resources. While these devices have several advantages, including continuous and dependable oxygen treatment, the initial purchase price and annual maintenance costs can be expensive. This price barrier may limit access for some healthcare institutions and individuals, preventing the widespread use of medical oxygen concentrators, particularly in economically poor regions.

Furthermore, logistical constraints associated with service and maintenance provide an additional constraint. Regular check-ups, filter changes, and technical troubleshooting necessitate a well-established after-sales service system. It might be difficult to ensure the appropriate operation and maintenance of medical oxygen concentrators in areas with poor healthcare infrastructure. This limitation not only has an influence on the efficiency of oxygen treatment, but it may also have an impact on the overall dependability and durability of these devices, impacting the market's growth potential in specific geographical locations.

Global Medical Oxygen Concentrators Market: Opportunities

Increasing awareness and acceptance of home healthcare solutions to provide growth opportunities

With a growing desire for at-home medical care, the demand for portable, user-friendly oxygen concentrators is on the rise. These innovative devices empower individuals with respiratory illnesses to take control of their therapy, reducing the need for hospital visits. This trend is not only driven by patient preference, but also by healthcare providers and insurance companies aiming to optimize resources and enhance patient well-being. As a result, manufacturers have a significant opportunity to develop new, compact, and user-friendly oxygen concentrators to meet the evolving landscape of home healthcare.

Additionally, technological advancements present another pathway for market growth in this industry. Ongoing R&D efforts are aimed at enhancing the efficiency and features of medical oxygen concentrators. Lightweight designs, longer battery life, and intelligent monitoring capabilities improve the entire user experience, making these devices more appealing to both healthcare practitioners and patients. Taking advantage of these technological options helps businesses to remain competitive, satisfy changing customer expectations, and contribute to the growth of the worldwide medical oxygen concentrators market.

Global Medical Oxygen Concentrators Market: Challenges

Limited access to electricity in certain regions to challenge market growth

The restricted access to energy in certain countries, which hinders the regular and uninterrupted use of these devices, is a key constraint in the worldwide medical oxygen concentrators market. Maintaining a constant supply of oxygen becomes difficult in locations with poor power infrastructure or frequent power outages. This can reduce the efficacy of oxygen therapy, particularly for patients who rely on medical oxygen concentrators to manage chronic respiratory disorders. To overcome this difficulty, creative solutions such as the development of resilient battery systems, alternative power sources, or strategic relationships with local utilities are required to assure a consistent power supply for this vital medical equipment. Regulatory barriers and compliance standards are also a difficulty for producers and distributors in the worldwide medical oxygen concentrators market.

Significant expenditures in quality assurance, testing, and certification systems are required due to stringent rules and differing compliance requirements across different areas. Meeting these regulatory criteria is critical for assuring medical oxygen concentrator safety and efficacy. Navigating the complicated regulatory structure necessitates significant resources and expertise, posing a challenge for market participants seeking to grow their worldwide footprint. To address these issues, a complete approach combining technology innovation, strategic alliances, and a full grasp of regional regulatory frameworks is required.

Global Medical Oxygen Concentrators Market: Segmentation

The global medical oxygen concentrators market is segmented based on product type, technology, application, and region.

Based on product type, the global industry segments are stationary oxygen concentrators, and portable oxygen concentrators. The stationary oxygen concentrators segment presently dominates the global market. This is owing to its broad use in clinical and home care settings. Stationary oxygen concentrators deliver a steady stream of concentrated oxygen and are appropriate for patients who require long-term oxygen therapy. Because of their rugged construction, increased oxygen production capacity, and ability to work continuously, they are a popular option in healthcare settings.

Based on application the global medical oxygen concentrators market categorized as continuous flow oxygen Concentrators, and pulse flow oxygen concentrators. In 2022, the worldwide market's largest shareholding sector was continuous flow oxygen concentrators. This dominance can be traced to the extensive usage of continuous flow models, particularly in clinical settings and situations requiring a consistent and constant supply of oxygen, such as hospitals and other healthcare institutions.

Based on application the global medical oxygen concentrators market categorized as home care, hospitals, and ambulatory surgical centers (ASCs). In 2022, the largest shareholder sector in the worldwide market was home care. This dominance is being driven by a growing trend toward home-based healthcare solutions, as patients prefer the ease and comfort of controlling their respiratory treatment at home.

Medical Oxygen Concentrators Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Medical Oxygen Concentrators Market |

| Market Size in 2022 | USD 3,552 Million |

| Market Forecast in 2030 | USD 8,112 Million |

| Growth Rate | CAGR of 6.2% |

| Number of Pages | 215 |

| Key Companies Covered | ResMed Inc., Philips Respironics, Invacare Corporation, Inogen Inc., Drive DeVilbiss Healthcare, Chart Industries, Nidek Medical Products Inc., Teijin Limited, Precision Medical Inc., GCE Group., and others. |

| Segments Covered | By Product Type, By Technology, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2022 |

| Historical Year | 2017 to 2021 |

| Forecast Year | 2023 - 2030 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Global Medical Oxygen Concentrators Market: Regional Analysis

Asia Pacific to lead the market during the forecast period

The Asia Pacific region is expected to dominate the global medical oxygen concentrators market in the coming years due to a multitude of significant factors. A rapidly aging population and a rise in respiratory illnesses have led to a surge in demand for reliable respiratory support systems. As countries like China and India invest in and expand their healthcare systems, there has been a corresponding rise in the adoption of medical oxygen concentrators to cater to the escalating respiratory needs of their populations. Moreover, the increasing recognition of at-home healthcare options and the emergence of compact and user-friendly oxygen concentrators are aligned with cultural preferences in various countries in the Asia Pacific region, stimulating the growth of the market.

In addition, with a focus on technological advancements and continuous product innovation in nations like Japan and South Korea, the region holds great importance in the global market for medical oxygen concentrators. As healthcare experts seek more effective and patient-centered solutions, the demand for cutting-edge oxygen concentrators is expected to rise. Due to its pivotal role in the international healthcare landscape, the Asia Pacific region is projected to be a major driving force in the medical oxygen concentrator market.

- Philips expands its Asia Pacific medical oxygen concentrator product offering with new models targeted for particular patient needs.

- Invacare forms alliances with local healthcare providers and distributors to expand its market reach in the region.

- AirSep Corporation invests in R&D to create new and patient-friendly medical oxygen concentrators.

Key Developments

2022: ASI Group, a global toilet partitions producer, has acquired R.L. Wilson's commercial medical oxygen concentrators company, a prominent provider of metal toilet partitions. This purchase broadens ASI Group's product offering and solidifies the company's position as a leading global provider of Medical Oxygen Concentrators.

2021: Bradley Corporation, a renowned maker of commercial bathroom goods, has purchased H&E goods, a manufacturer of toilet partitions, lockers, and other washroom accessories. Bradley's portfolio now includes H&E Products' expertise in manufacturing high-density polyethylene (HDPE) partitions.

Global Medical Oxygen Concentrators Market: Competitive Analysis

The global medical oxygen concentrators market is dominated by players like:

- ResMed Inc.

- Philips Respironics (a division of Royal Philips)

- Invacare Corporation

- Inogen Inc.

- Drive DeVilbiss Healthcare

- Chart Industries

- Nidek Medical Products Inc.

- Teijin Limited

- Precision Medical, Inc.

- GCE Group

The global medical oxygen concentrators market is segmented as follows:

By Product Type

- Stationary Oxygen Concentrators

- Portable Oxygen Concentrators

By Technology

- Continuous Flow Oxygen Concentrators

- Pulse Flow Oxygen Concentrators

By Application

- Home Care

- Hospitals

- Ambulatory Surgical Centers (ASCs))

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

Medical oxygen concentrators are vital respiratory devices that serve a critical role in giving concentrated oxygen to those who have difficulty breathing. These machines work by pulling in room air, filtering out contaminants, and delivering a constant stream of pure oxygen to patients via masks or nasal cannulas.

The global medical oxygen concentrator’s market cap may grow owing to the due to the increased frequency of respiratory illnesses, along with an aging population, is boosting demand for dependable respiratory support equipment.

According to study, the global medical oxygen concentrator’s market size was worth around USD 3,552 million in 2022 and is predicted to grow to around USD 8,112 million by 2030.

The CAGR value of the global medical oxygen concentrators market is expected to be around 6.2% during 2023-2030.

The global medical oxygen concentrator’s market growth is expected to be driven by Asia Pacific. It is currently the world’s highest revenue-generating market owing to region's growing aging population, coupled with a rising prevalence of respiratory disorders.

The global medical oxygen concentrators market is led by players like ResMed Inc., Philips Respironics, Invacare Corporation, Inogen Inc., Drive DeVilbiss Healthcare, Chart Industries, Nidek Medical Products Inc., Teijin Limited, Precision Medical, Inc., and GCE Group.

The report analyzes the global medical oxygen concentrators market’s drivers, restraints/challenges, and the effect they have on the demands during the projection period. In addition, the report explores emerging opportunities in the medical oxygen concentrators industry.

Choose License Type

List of Contents

Medical Oxygen ConcentratorsIndustry Prospective:GlobalOverviewKey InsightsGlobalGrowth DriversGlobalRestraintsGlobalOpportunitiesGlobalChallengesGlobalSegmentationMedical Oxygen Concentrators Report ScopeGlobalRegional AnalysisKey DevelopmentsGlobalCompetitive AnalysisThe global medical oxygen concentrators market is segmented as follows:By RegionRelatedNews

Zion Market Research

Tel: +1 (302) 444-0166

USA/Canada Toll Free No.+1 (855) 465-4651

3rd Floor,

Mrunal Paradise, Opp Maharaja Hotel,

Pimple Gurav, Pune 411061,

Maharashtra, India

Phone No +91 7768 006 007, +91 7768 006 008

US OFFICE NO +1 (302) 444-0166

US/CAN TOLL FREE +1 (855) 465-4651

Email: sales@zionmarketresearch.com

We have secured system to process your transaction.

Our support available to help you 24 hours a day, five days a week.

Monday - Friday: 9AM - 6PM

Saturday - Sunday: Closed