Oncology Companion Diagnostic Market Size, Share, Trends, Growth and Forecast 2032

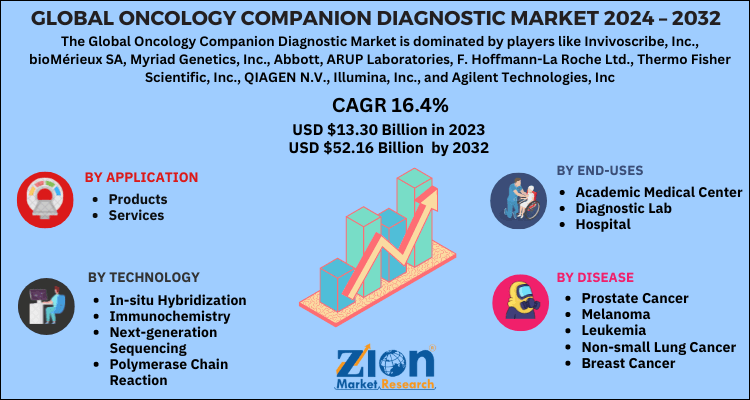

Oncology Companion Diagnostic Market By Application (products and services), By Technology (in-situ hybridization, immunochemistry, next-generation sequencing, and polymerase chain reaction), By Disease (prostate cancer, melanoma, leukemia, non-small lung cancer, and breast cancer), By End-uses (academic medical center, diagnostic lab, and hospital) And By Region: - Global And Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, And Forecasts, 2024-2032

| Market Size in 2023 | Market Forecast in 2032 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 13.30 Billion | USD 52.16 Billion | 16.4% | 2023 |

Description

Oncology Companion Diagnostic Market Insights

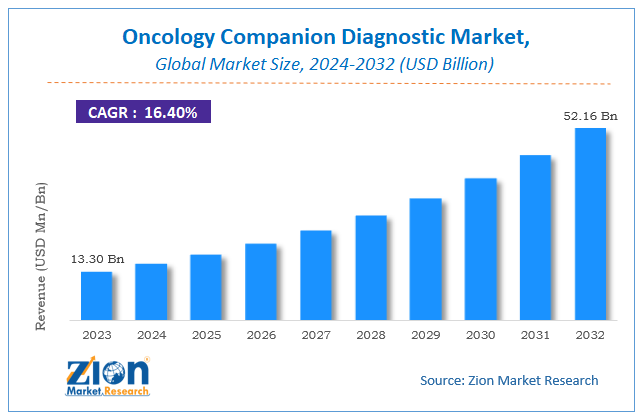

According to the report published by Zion Market Research, the global Oncology Companion Diagnostic Market size was valued at USD 13.30 Billion in 2023 and is predicted to reach USD 52.16 Billion by the end of 2032. The market is expected to grow with a CAGR of 16.4% during the forecast period. The report analyzes the global Oncology Companion Diagnostic Market's growth drivers, restraints, and impact on demand during the forecast period. It will also help navigate and explore the arising opportunities in the Oncology Companion Diagnostic industry.

Global Oncology Companion Diagnostic Market: Overview

Companion diagnostics along with drugs are developed to aid in the selection or exclusion of groups to that of the patient with selected drugs, depending on the biological characteristics of the patient.

The resulting characteristics of a patient determine and differentiate them as non-responders and responders to the therapy. The oncology diagnostics assays are able to reduce the number of clinical trials and thus enhance the adoption rates of this CDx by pharma companies.

Global Oncology Companion Diagnostic Market: Growth Factors

The emerging utilization of oncology companion diagnostics in the next generation of omics is anticipated to drive the market growth. Diagnostics co-development along with drugs is improved with in-vitro companion diagnostics devices guide issued by the FDA. This is also emphasizing the diagnostic assay approval along with its therapeutic products.

Contemporaneously, it aligned the research and development activities between various leading companies. It assists in selecting the lead compound with corresponding biomarkers from diagnostic and pharmaceutical manufacturers to collaborate and efficiently develop oncology companion and drug assays.

FDA approval of Ventana HER2 dual ISH DNA probe cocktail assay has enabled the development of a fast novel method for examination of HER2 biomarkers to diagnose breast cancer. This development is significantly boosting the global oncology companion diagnostic market.

Key Insights

- As per the analysis shared by our research analyst, the global Oncology Companion Diagnostic Market is estimated to grow annually at a CAGR of around 16.4% over the forecast period (2024-2032).

- In terms of revenue, the global Oncology Companion Diagnostic Market size was valued at around USD 13.30 Billion in 2023 and is projected to reach USD 52.16 Billion by 2032.

- Based on the application, Products this segment, encompassing instruments, consumables, and software, dominated the market with a 66.32% share in 2023. The growth is driven by advancements in personalized medicine and the increasing prevalence of cancer.

- Based on the technology, Polymerase Chain Reaction (PCR) holding a 22.19% market share in 2023, PCR's dominance is due to its high specificity and sensitivity in cancer diagnosis. Real-time PCR assays are particularly favored for analyzing cancer markers.

- Based on the disease, Non-Small Cell Lung Cancer (NSCLC) this segment led with a 30.13% share in 2023, attributed to the high incidence of NSCLC globally, necessitating effective companion diagnostics for targeted therapies.

- Based on the end-uses, the Hospitals dominated the market with a 52.11% share in 2023. The wide array of cancer diagnostic tests and the increasing adoption of advanced diagnostics contribute to this dominance.

- Based on the region, North America leading the market with approximately 40% of the total revenue in 2023, North America's dominance is driven by advanced healthcare infrastructure and significant investments in personalized medicine.

Oncology Companion Diagnostic Market: Dynamics

Key Growth Drivers

The oncology companion diagnostic market is primarily driven by the rising prevalence of cancer worldwide and the growing emphasis on personalized medicine. Companion diagnostics play a critical role in identifying patients who are most likely to benefit from targeted therapies, improving treatment outcomes and reducing adverse effects. Advances in genomic research and biomarker identification further fuel market growth by enabling the development of more effective and precise diagnostic tools. Additionally, increasing collaboration between pharmaceutical companies and diagnostic manufacturers to co-develop targeted therapies and companion diagnostics supports market expansion. Government initiatives promoting precision medicine and regulatory approvals for new diagnostic tests further accelerate growth.

Restraints

Despite its growth potential, the oncology companion diagnostic market faces challenges due to the high cost of developing and validating these diagnostic tests. The complex regulatory approval processes for companion diagnostics and their corresponding therapies can result in significant delays and additional expenses. Limited access to advanced diagnostic technologies in developing regions also restricts market growth. Furthermore, the requirement for specialized laboratories and skilled professionals to conduct diagnostic testing adds to operational challenges. In some cases, the lack of reimbursement policies for companion diagnostics can deter their adoption, particularly in cost-sensitive healthcare systems.

Opportunities

The increasing adoption of next-generation sequencing (NGS) and liquid biopsy technologies presents lucrative opportunities in the oncology companion diagnostic market. These advanced diagnostic techniques offer non-invasive and comprehensive tumor profiling, facilitating early cancer detection and personalized treatment decisions. Expanding research into novel cancer biomarkers and the development of multi-gene panel tests also enhance the market's growth potential. Additionally, the integration of artificial intelligence (AI) and machine learning algorithms in diagnostic platforms enables more accurate and faster data analysis. Emerging markets with growing healthcare infrastructure investments provide further opportunities for market expansion, especially with rising awareness of precision oncology.

Challenges

One of the major challenges in the oncology companion diagnostic market is ensuring the clinical validity and reliability of diagnostic tests across diverse patient populations. Variations in genetic profiles and tumor heterogeneity can impact the accuracy and effectiveness of companion diagnostics. Moreover, the need for continuous updates and validation of diagnostic assays to keep pace with evolving cancer therapies adds complexity for manufacturers. Fragmented regulatory frameworks across different regions can further delay product approvals and market entry. Additionally, limited patient access to advanced diagnostic solutions, particularly in rural and underserved areas, remains a significant barrier to market growth.

Oncology Companion Diagnostic Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Oncology Companion Diagnostic Market |

| Market Size in 2023 | USD 13.30 Billion |

| Market Forecast in 2032 | USD 52.16 Billion |

| Growth Rate | CAGR of 16.4% |

| Number of Pages | 201 |

| Key Companies Covered | Invivoscribe, Inc., bioMérieux SA, Myriad Genetics, Inc., Abbott, ARUP Laboratories, F. Hoffmann-La Roche Ltd., Thermo Fisher Scientific, Inc., QIAGEN N.V., Illumina, Inc., and Agilent Technologies, Inc |

| Segments Covered | By Application, By Technology, By Disease, By End-uses And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2022 |

| Forecast Year | 2024 - 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Global Oncology Companion Diagnostic Market: Segmentation

The real-time polymerase chain reaction (PCR), in-situ hybridization(ISH) technologies, and immunohistochemistry are the traditional methods of diagnosing disease biomarkers.

But the emergence of sensitive approaches like single-molecule real-time leaf time sequencing, quantitative histopathology, next-generation sequencing, and digital pathology are gradually shifting the medical approaches to CDx technology to efficiently detect the diseases and thus are driving the market growth significantly.

The global oncology companion diagnostic market can be segmented into application, technology, disease, end-uses, and region. All the segments have been analyzed based on present and future trends and the market is estimated from 2024 to 2032.

By application, the market can be segmented into products and services.

The product segment holds the largest share in the global oncology companion diagnostic market. The segment is expected to witness healthy growth over the forecast period owing to the development of highly sensitive technologies like NGS.

The product segment can be further classified into the instrument, software, and consumables

Consumables are important in cancer testing as they provide more reliable results. Many leading companies are engaging in the development of consumables owing to its growing scope.

By technology, the market can be segmented into in-situ hybridization, immunochemistry, next-generation sequencing, and polymerase chain reaction.

Immunochemistry (IHC) holds the largest share in the global oncology companion diagnostic market. Its growth is attributed to the growing scope and availability of IHC-based companion diagnostic assays. Indulgence of key players to promote the product launch and approval has accelerated the market growth.

The next-generation sequencing is expected to grow significantly during the forecast period due to precise and detailed results on the biomarker.

By disease, the market can be segmented into prostate cancer, melanoma, leukemia, non-small lung cancer, and breast cancer.

The non-small lung cancer (NSCLC) segment is dominating the market and is expected to grow further during the forecast years due to the high incidence of cases of NSCLC.

By end-use, the market can be segmented into the academic medical center, diagnostic lab, and hospital.

The regional segment includes the current and forecast demand for North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

The hospital segment is dominating the market due to the increasing rate of penetration of companion diagnostics in hospitals.

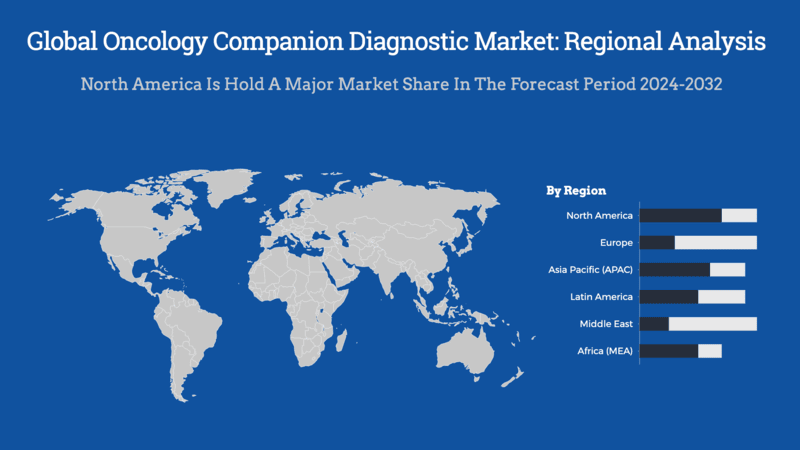

Global Oncology Companion Diagnostic Market: Regional analysis

North America holds the largest market share in the global oncology companion diagnostic market owing to the accelerated development of precision therapy in the region and increased promotion of novel products & technology for detection, promotion, and treatment of cancer.

The oncology companion diagnostic market demonstrates distinct regional dynamics influenced by healthcare infrastructure, cancer prevalence, and technological advancements.

North America

North America leads the market, accounting for approximately 40% of the global revenue in 2023. This dominance is attributed to advanced healthcare infrastructure, substantial healthcare expenditure, and the presence of leading research institutions and biotechnology firms dedicated to developing innovative diagnostic methods. The robust regulatory framework in the region ensures timely approval and commercialization of new diagnostic tools.

Europe

Europe holds a significant share of the global market, driven by developed economies such as Germany, the UK, France, and Italy. These countries boast advanced healthcare infrastructures that enhance clinical research prospects. Strategic collaborations and the introduction of innovative products further contribute to market growth. For instance, partnerships aimed at offering in-house genomic testing for cancer patients have been established in France, enhancing diagnostic precision and personalized treatment options.

Asia-Pacific

The Asia-Pacific region is projected to experience the fastest growth rate over the forecast period. Factors such as healthcare reforms, enhanced infrastructure, a growing population, and an increasing number of local companies entering the market drive this expansion. Notably, nearly half of all global cancer cases and approximately 56.1% of cancer deaths in 2022 were reported in Asia, underscoring the urgent need for effective diagnostic solutions. Countries like China and Japan are focusing on developing new therapies and investing in government initiatives to reduce cancer incidence.

Latin America

Latin America is identified as a lucrative region within this market, experiencing significant growth in precision medicine technology, driven by various initiatives to boost research and development. Collaborations among pharmaceutical companies, diagnostics firms, and service providers are enhancing access to precision medicine technologies. In Brazil, advancements in genetic testing technologies and a growing emphasis on precision medicine, supported by collaborations between global innovators and local healthcare providers, are propelling market growth.

Middle East and Africa

The Middle East and Africa present significant growth opportunities, though the market remains largely untapped due to the absence of structured cancer screening programs in underdeveloped African economies, which has impeded early detection efforts. In Saudi Arabia, increasing government involvement and rising awareness about the benefits of noninvasive diagnostic procedures are expected to drive market growth over the forecast period.

Global Oncology Companion Diagnostic Market: Competitive Players

Some of the leading players in the global oncology companion diagnostic market are:

- Invivoscribe, Inc.

- bioMérieux SA

- Myriad Genetics, Inc.

- Abbott

- ARUP Laboratories

- F. Hoffmann-La Roche Ltd.

- Thermo Fisher Scientific, Inc.

- QIAGEN N.V., Illumina, Inc.

- Agilent Technologies, Inc.

The Global Oncology Companion Diagnostic Market is segmented as follows:

By Application

- products

- services

By Technology

- in-situ hybridization

- immunochemistry

- next-generation sequencing

- polymerase chain reaction

By Disease

- prostate cancer

- melanoma

- leukemia

- non-small lung cancer

- breast cancer

By End-uses

- academic medical center

- diagnostic lab

- hospital

Global Oncology Companion Diagnostic Market: Regional Segment Analysis

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

What Reports Provides

- Full in-depth analysis of the parent market

- Important changes in market dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional markets

- Testimonials to companies in order to fortify their foothold in the market.

Table Of Content

Choose License Type

Zion Market Research

Tel: +1 (302) 444-0166

USA/Canada Toll Free No.+1 (855) 465-4651

3rd Floor,

Mrunal Paradise, Opp Maharaja Hotel,

Pimple Gurav, Pune 411061,

Maharashtra, India

Phone No +91 7768 006 007, +91 7768 006 008

US OFFICE NO +1 (302) 444-0166

US/CAN TOLL FREE +1 (855) 465-4651

Email: sales@zionmarketresearch.com

We have secured system to process your transaction.

Our support available to help you 24 hours a day, five days a week.

Monday - Friday: 9AM - 6PM

Saturday - Sunday: Closed