Pancreatic Cancer Treatment Market Size, Share, Trends, Growth and Forecast 2034

Pancreatic Cancer Treatment Market By Type (Exocrine and Endocrine), By Treatment Type (Chemotherapy, Targeted Therapy, Immunotherapy, Radiation Therapy, and Others), By Distribution Channel (Hospitals, Specialty Clinics, Research Institutes, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

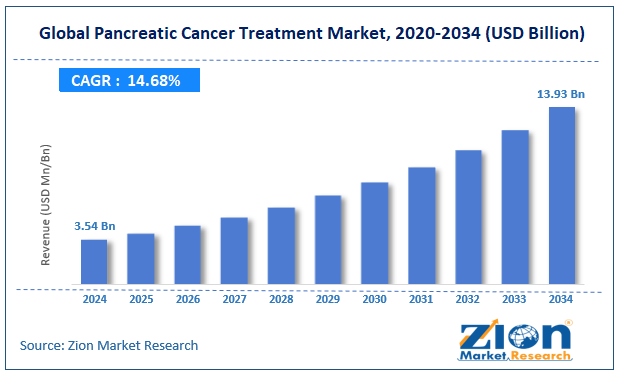

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 3.54 Billion | USD 13.93 Billion | 14.68% | 2024 |

Pancreatic Cancer Treatment Industry Prospective:

The global pancreatic cancer treatment market size was valued at approximately USD 3.54 billion in 2024 and is expected to reach around USD 13.93 billion by 2034, growing at a compound annual growth rate (CAGR) of roughly 14.68% between 2025 and 2034.

Pancreatic Cancer Treatment Market: Overview

Pancreatic cancer is a malignant disease that originates in the tissues of the pancreas, an organ responsible for aiding digestion and regulating blood sugar levels. It originates in the pancreatic tissues, primarily affecting the exocrine and endocrine functions of the organ.

Due to its poor prognosis and limited treatment options, there has been a growing emphasis on innovative therapies, including targeted therapy, immunotherapy, and novel drug combinations. Advances in precision medicine, biomarker-based treatment approaches, and minimally invasive surgical techniques are reshaping the landscape of pancreatic cancer management.

Ongoing genetic predisposition and molecular profiling research further enhance personalized treatment strategies for better patient outcomes. Early detection remains challenging, as symptoms often appear in advanced stages, making timely diagnosis crucial for improving survival rates.

The increasing incidence of the disease, coupled with technological advancements in treatment methodologies, is expected to drive significant market growth over the forecast period.

Key Insights:

- The global pancreatic cancer treatment market is anticipated to grow at a CAGR of 14.68% from 2025 to 2034.

- The market was valued at around USD 3.54 billion in 2024 and is projected to reach USD 13.93 billion by 2034.

- Rising incidence of pancreatic cancer, increasing healthcare expenditures, and advancements in targeted therapies are key drivers of the pancreatic cancer treatment market.

- Based on therapy type, chemotherapy remains the most commonly utilized treatment, while targeted therapy is gaining traction due to its promising clinical outcomes.

- Based on type, exocrine pancreatic cancer leads the treatment market as it accounts for over 90% of cases.

- Based on the distribution channel, hospitals dominate by offering integrated, multidisciplinary cancer care under one roof.

- North America is expected to dominate the market, followed by Europe, Asia-Pacific, and Latin America.

Pancreatic Cancer Treatment Market: Growth Drivers

Advancements in Targeted and Immunotherapy-Based Treatments

The shift from conventional chemotherapy to precision medicine is significantly impacting the pancreatic cancer treatment market. Targeted therapies such as PARP inhibitors and immunotherapies like immune checkpoint inhibitors demonstrate improved survival rates in clinical trials.

For instance, the FDA-approved drug Olaparib has shown efficacy in treating BRCA-mutated pancreatic cancer patients, offering a promising alternative to traditional treatments. Additionally, ongoing research into biomarker-driven therapies expands personalized treatment options, enhances patient outcomes, and further accelerates market growth.

Government Initiatives and Increased Research Funding

Several governments and healthcare organizations invest heavily in cancer research to develop novel treatments and early detection techniques.

The U.S. National Cancer Institute (NCI) allocated over USD 300 million in 2024 for pancreatic cancer research, fostering the development of breakthrough therapies and diagnostic tools. Similar initiatives in Europe and Asia-Pacific are expected to enhance treatment accessibility and affordability.

Pancreatic Cancer Treatment Market: Restraints

High Treatment Costs and Limited Accessibility

Pancreatic cancer treatment remains expensive due to the high cost of novel therapies, diagnostic procedures, and hospital stays. Many emerging economies face challenges in accessing advanced treatments, leading to disparities in patient outcomes.

Additionally, insurance coverage limitations and reimbursement issues further restrict market growth. The limited availability of specialized treatment centers and expertise in certain regions also hinders timely diagnosis and access to optimal care.

Poor Prognosis and Resistance to Therapies

Despite advancements in treatment, pancreatic cancer continues to have a poor survival rate due to late-stage diagnosis and resistance to standard therapies. The five-year survival rate remains below 10%, making developing more effective and personalized treatment approaches imperative. Limited awareness and the lack of reliable early screening methods contribute to delayed diagnoses, further worsening patient outcomes.

Pancreatic Cancer Treatment Market: Opportunities

Emerging Role of Liquid Biopsy and Personalized Medicine

Integrating liquid biopsy techniques for early diagnosis and treatment monitoring is revolutionizing pancreatic cancer management. Companies focus on developing non-invasive diagnostic tests that enable timely intervention and personalized treatment regimens.

Advancements in genomic sequencing are also opening new avenues for patient-specific therapeutic approaches. These innovations improve early detection rates, reduce reliance on invasive procedures, and drive precision oncology adoption in pancreatic cancer care.

Expanding Clinical Trials and Drug Development Pipelines

Several pharmaceutical companies are investing in clinical trials to explore novel drug combinations and immunotherapies. The success of trials focusing on combination therapies, such as checkpoint inhibitors with chemotherapy, is expected to reshape the treatment paradigm and expand opportunities for the pancreatic cancer treatment industry.

Positive trial outcomes accelerate regulatory approvals, increase treatment options, and drive further investment in innovative pancreatic cancer therapies.

Pancreatic Cancer Treatment Market: Challenges

Regulatory Hurdles and Long Approval Processes

The stringent regulatory landscape for new drug approvals presents a significant challenge for pancreatic cancer treatment market players. Clinical trials for pancreatic cancer treatments often require extensive time and financial resources, delaying the availability of innovative drugs.

Regulatory hurdles and lengthy clinical trial processes slow the approval of new pancreatic cancer treatments. High costs and stringent requirements further challenge market expansion. The need for comprehensive safety and efficacy data adds to the complexity, making it difficult for smaller biotech firms to enter the market.

Pancreatic Cancer Treatment Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Pancreatic Cancer Treatment Market |

| Market Size in 2024 | USD 3.54 Billion |

| Market Forecast in 2034 | USD 13.93 Billion |

| Growth Rate | CAGR of 14.68% |

| Number of Pages | 224 |

| Key Companies Covered | Roche Holding AG, Novartis AG, Pfizer Inc., Bristol-Myers Squibb Company, Eli Lilly and Company, AstraZeneca PLC, Merck & Co. Inc., Amgen Inc., Celgene Corporation, Ipsen S.A., GlaxoSmithKline plc, Bayer AG, Johnson & Johnson, Sanofi, AbbVie Inc., and others. |

| Segments Covered | By Type, By Treatment Type, By Distribution channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Pancreatic Cancer Treatment Market: Segmentation

The global pancreatic cancer treatment market is segmented based on type, treatment type, distribution channel, and region.

Based on type, the pancreatic cancer treatment industry is segregated into exocrine and endocrine. Exocrine pancreatic cancer leads the market as it accounts for over 90% of cases, primarily pancreatic ductal adenocarcinoma (PDAC), which is aggressive and often diagnosed late. Additionally, this drives demand for chemotherapy and targeted therapies.

Based on treatment type, the market is divided into chemotherapy, targeted therapy, immunotherapy, radiation therapy, and others. Chemotherapy leads the pancreatic cancer treatment industry as it remains the first-line standard of care, especially for advanced and metastatic cases. Additionally, combination regimens like FOLFIRINOX and gemcitabine-based therapies offer enhanced efficacy, further reinforcing chemotherapy’s leading position.

Based on distribution channels, the market is categorized into hospitals, specialty clinics, research institutes, and others. Hospitals dominate the market by providing multidisciplinary cancer care, integrating surgery, chemotherapy, radiation, and supportive treatments under one roof. Their advanced infrastructure, access to specialized oncologists, and availability of clinical trials make them the preferred choice for standard and cutting-edge therapies.

Pancreatic Cancer Treatment Market: Regional Analysis

North America to Lead the Market

North America is expected to dominate the global pancreatic cancer treatment market due to the presence of advanced healthcare infrastructure, high investment in cancer research, and strong governmental support. The U.S. has the largest market share, driven by increased adoption of novel therapies and a growing patient pool.

Major pharmaceutical companies in the region are actively involved in clinical trials and drug development, accelerating the approval and commercialization of advanced treatments.

Additionally, favorable reimbursement policies and healthcare expenditures improve accessibility to innovative therapies. The rising prevalence of pancreatic cancer cases in the U.S. and Canada, combined with increased awareness programs, further strengthens market expansion.

The region also benefits from collaborations between research institutions and biotech firms, fostering innovation and speeding up the development of breakthrough therapies.

Europe to Witness Significant Growth

Europe is experiencing robust growth in the pancreatic cancer treatment industry, with key contributions from Germany, the UK, France, and Italy. The region benefits from strong governmental support in cancer research and improved access to cutting-edge therapies.

Regulatory bodies like the European Medicines Agency (EMA) are crucial in fast-tracking approvals for innovative treatments. The increasing focus on early diagnosis, precision medicine, and clinical trial participation in European countries further drives market expansion.

The presence of leading biotech firms and collaborations between research institutes and pharmaceutical companies enhance the development of novel therapies. Additionally, a growing elderly population and lifestyle-related risk factors contribute to a rising incidence of pancreatic cancer.

Recent Market Developments:

- In March 2024, the FDA approved a new targeted therapy for pancreatic cancer, demonstrating a 20% increase in progression-free survival.

- In June 2024, Roche announced promising results from its Phase III trial combining immunotherapy with chemotherapy.

- In August 2024, Pfizer partnered with a leading research institute to develop AI-driven precision medicine approaches for pancreatic cancer treatment.

- In October 2024, a UK-based biotech company, Xgenera, launched a novel liquid biopsy test for early pancreatic cancer detection, improving diagnostic accuracy by 40%.

- In December 2024, Eli Lilly secured fast-track designation from the FDA for its novel combination therapy, aiming to improve survival rates in late-stage pancreatic cancer patients.

Pancreatic Cancer Treatment Market: Competitive Analysis

The global pancreatic cancer treatment market is led by players like:

- Roche Holding AG

- Novartis AG

- Pfizer Inc.

- Bristol-Myers Squibb Company

- Eli Lilly and Company

- AstraZeneca PLC

- Merck & Co. Inc.

- Amgen Inc.

- Celgene Corporation

- Ipsen S.A.

- GlaxoSmithKline plc

- Bayer AG

- Johnson & Johnson

- Sanofi

- AbbVie Inc.

The global pancreatic cancer treatment market is segmented as follows:

By Type

- Endocrine

- Exocrine

By Treatment Type

- Chemotherapy

- Targeted therapy

- Immunotherapy

- Radiation therapy

- Others.

By Distribution channel

- Hospitals

- Specialty clinics

- Research institutes

- Others.

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

Pancreatic cancer is a malignant disease that originates in the tissues of the pancreas, an organ responsible for aiding digestion and regulating blood sugar levels. It originates in the pancreatic tissues, primarily affecting the exocrine and endocrine functions of the organ.

The pancreatic cancer treatment market is expected to be driven by advancements in targeted and immunotherapy-based treatments, government initiatives, and increased research funding.

According to market research, the global pancreatic cancer treatment market was valued at approximately USD 3.54 billion in 2024 and is projected to reach around USD 13.93 billion by 2034, driven by innovative therapies and improved early detection techniques.

The pancreatic cancer treatment market is expected to grow at a compound annual growth rate (CAGR) of approximately 14.68% from 2025 to 2034, fueled by advancements in treatment methodologies and increased healthcare expenditure worldwide.

North America is expected to dominate the global pancreatic cancer treatment market due to the presence of advanced healthcare infrastructure, high investment in cancer research, and strong governmental support.

Key players in the pancreatic cancer treatment market include Roche Holding AG, Novartis AG, Pfizer Inc., Bristol-Myers Squibb Company, Eli Lilly and Company, AstraZeneca PLC, Merck & Co., Inc., Amgen Inc., Celgene Corporation, Ipsen S.A., GlaxoSmithKline plc, Bayer AG, Johnson & Johnson, Sanofi, and AbbVie Inc.

The report provides a comprehensive analysis of the pancreatic cancer treatment market, including an in-depth discussion of market drivers, restraints, emerging treatment trends, regulatory landscapes, and future growth opportunities. It also examines competitive dynamics, regional market performance, and ongoing clinical advancements in targeted and immunotherapy-based treatments.

Zion Market Research

Tel: +1 (302) 444-0166

USA/Canada Toll Free No.+1 (855) 465-4651

3rd Floor,

Mrunal Paradise, Opp Maharaja Hotel,

Pimple Gurav, Pune 411061,

Maharashtra, India

Phone No +91 7768 006 007, +91 7768 006 008

US OFFICE NO +1 (302) 444-0166

US/CAN TOLL FREE +1 (855) 465-4651

Email: sales@zionmarketresearch.com

We have secured system to process your transaction.

Our support available to help you 24 hours a day, five days a week.

Monday - Friday: 9AM - 6PM

Saturday - Sunday: Closed