Semiconductor Fabrication Material Market Size, Share, Trends, Growth 2032

Semiconductor Fabrication Material Market By Material (Silicon Wafers, Photomasks, Photoresists, Wet Chemicals, CMP Slurry and Pads, Gases, Sputter Targets, and Photoresist Ancillaries), By Application (Consumer Appliances, Power Generation, Electronic Components, and Others), By Industry Vertical (Telecommunication, Energy, Electrical & Electronics, Medical & Healthcare, Automotive, and Others), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2024 - 2032

| Market Size in 2023 | Market Forecast in 2032 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 55.9 Billion | USD 98.5 Billion | 6.5% | 2023 |

Semiconductor Fabrication Material Industry Prospective:

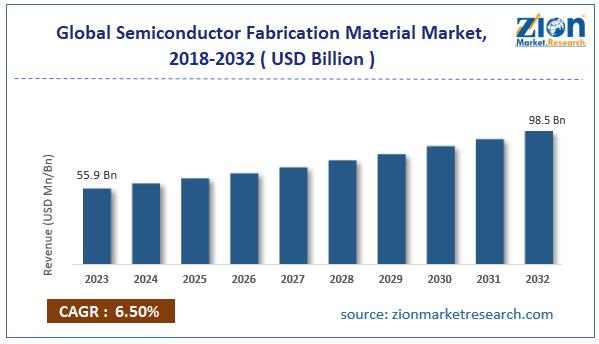

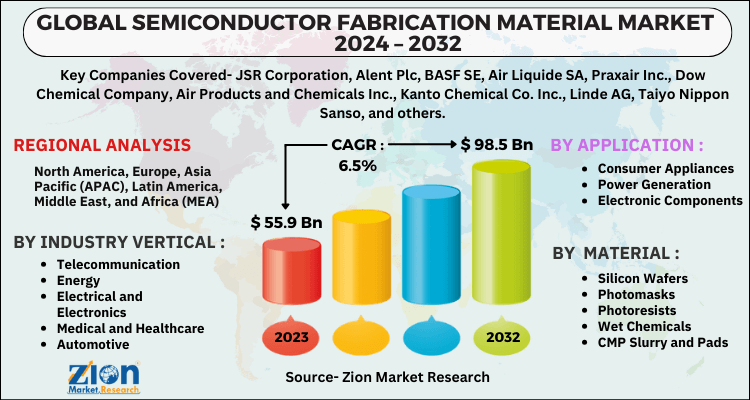

The global semiconductor fabrication material market size was worth around USD 55.9 billion in 2023 and is predicted to grow to around USD 98.5 billion by 2032 with a compound annual growth rate (CAGR) of roughly 6.5% between 2024 and 2032.

Semiconductor Fabrication Material Market: Overview

Semiconductor fabrication materials are the raw components and elements employed in the fabrication and production of semiconductor devices, such as integrated circuits (ICs) and microchips. From wafer fabrication to device assembly and packaging, these components are vital in several phases of semiconductor processing. The components chosen must satisfy exact standards for performance, accuracy, and purity.

High-performance semiconductors used in everything from consumer electronics to industrial and automotive systems depend on these materials to a significant extent. The semiconductor fabrication material market is being driven by several factors, such as increasing demand for semiconductors, technological advancements, growth in the automotive industry, increasing expansion of 5G networks, and many others.

Key Insights

- As per the analysis shared by our research analyst, the global semiconductor fabrication material market is estimated to grow annually at a CAGR of around 6.5% over the forecast period (2024-2032).

- In terms of revenue, the global semiconductor fabrication material market size was valued at around USD 55.9 billion in 2023 and is projected to reach USD 98.5 billion by 2032.

- The increasing consumer electronics industry is expected to drive the semiconductor fabrication material market over the forecast period.

- Based on material, the silicon wafers segment is expected to dominate the semiconductor fabrication material market over the forecast period.

- Based on application, the consumer appliances segment is expected to hold the largest market share over the forecast period.

- Based on industry vertical, the telecommunication segment is expected to hold the largest market share over the forecast period.

- Based on region, the Asia Pacific is expected to dominate the market during the forecast period.

Semiconductor Fabrication Material Market: Growth Drivers

Increasing demand for semiconductors drives market growth

The growing demand for semiconductors directly influences the semiconductor fabrication material market. Since almost every element of modern life depends on semiconductor-based devices, the demand for these materials, which are necessary for making semiconductors, has witnessed a tremendous increase.

Globally, consumer electronics, including wearables, computers, tablets, cellphones, and other demands are still rising. The core of these devices are semiconductors; as demand for more sophisticated, quicker, and energy-efficient electronics rises, so does demand for semiconductor fabrication materials like advanced chemicals, silicon wafers, and photoresists. Furthermore, a major driver of semiconductor demand is the automotive sector, especially because of the emergence of electric cars (EVs) and autonomous cars.

Semiconductor Fabrication Material Market: Restraints

The high cost of raw materials hinders market growth

The expansion of the semiconductor fabrication material industry is limited by the high prices of raw materials. Raw material prices directly affect semiconductor manufacturers' whole cost structure, therefore affecting production efficiency as well as market pricing. Rising prices of these materials result from several elements influencing the dynamics and expansion of the semiconductor manufacturing material market. Costful semiconductor fabrication materials include photoresists, high-purity silicon, rare-earth metals (e.g., cobalt, tantalum, tungsten), and specialty chemicals.

Although sophisticated semiconductors are created from these materials, their high prices help to drive higher manufacturing costs. Rising material costs may force producers to pass these expenses to consumers, therefore affecting the prices of finished semiconductor products and maybe reducing demand.

Semiconductor Fabrication Material Market: Opportunities

Growing investment offers a lucrative opportunity for market growth

The increasing investment is expected to offer a lucrative opportunity for the expansion of the semiconductor fabrication material market during the forecast period. For instance, in May 2023, Applied Materials, Inc. revealed a historic investment to create the biggest and most sophisticated center for joint semiconductor process technology and production equipment research and development (R&D). Designed to hasten the development and commercialization of the fundamental technologies required by the worldwide semiconductor and computer sectors, the new Equipment and Process Innovation and Commercialization (EPIC) Center is slated as the center of a high-velocity innovation platform.

Designed to offer a breadth and scale of capabilities unique in the industry, including more than 180,000 square feet – more than three American football fields – of state-of-the-art cleanroom for collaborative innovation with chipmakers, universities, and ecosystem partners, the multibillion-dollar facility is set to be housed at an Applied campus in Silicon Valley. Designed from the ground up to hasten the speed of introducing new manufacturing innovations, the new EPIC Center is expected to lower the time it takes the industry to bring a technology from concept to commercialization by several years while simultaneously raising the commercial success rate of innovations and the return on R&D investments for the entire semiconductor ecosystem.

Semiconductor Fabrication Material Market: Challenges

The complexity of manufacturing process poses a major challenge to market expansion

The production of semiconductors necessitates extremely accurate procedures and advanced machinery. For many manufacturers, scaling production effectively is difficult due to the complexity of developing advanced semiconductors (such as 7nm, 5nm, and lower nodes) and related materials. The cost is also influenced by the high degree of precision required in the handling and processing of materials. Therefore, the complexity of the manufacturing process poses a major challenge to the semiconductor fabrication material industry growth.

Request Free Sample

Request Free Sample

Semiconductor Fabrication Material Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Semiconductor Fabrication Material Market |

| Market Size in 2023 | USD 55.9 Billion |

| Market Forecast in 2032 | USD 98.5 Billion |

| Growth Rate | CAGR of 6.5% |

| Number of Pages | 221 |

| Key Companies Covered | JSR Corporation, Alent Plc, BASF SE, Air Liquide SA, Praxair Inc., Dow Chemical Company, Air Products and Chemicals Inc., Kanto Chemical Co. Inc., Linde AG, Taiyo Nippon Sanso, and others. |

| Segments Covered | By Material, By Application, By Industry Vertical, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2022 |

| Forecast Year | 2024 - 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Semiconductor Fabrication Material Market: Segmentation

The global semiconductor fabrication material industry is segmented based on material, application, industry vertical, and region.

Based on material, the global semiconductor fabrication material market is segmented into silicon wafers, photomasks, photoresists, wet chemicals, CMP slurry and pads, gases, sputter targets, and photoresist ancillaries. The silicon wafers segment is expected to dominate the semiconductor fabrication material market over the forecast period. Advanced semiconductor technology is used more and more in the automotive sector for features like infotainment systems, electric vehicles (EVs), autonomous driving, and safety measures. To produce semiconductors for various uses, silicon wafers are utilized. Revenue in the automotive electronics sector has increased as a result of the growing demand for silicon wafers, particularly with the development of EVs and smart car technology.

Based on application, the global semiconductor fabrication material industry is bifurcated into consumer appliances, power generation, electronic components, and others. The consumer appliances segment is expected to hold the largest market share over the forecast period. The need for semiconductors has increased due to the growing popularity of smart home appliances, such as smart air purifiers, dishwashers, washing machines, refrigerators, thermostats, and security systems.

Based on industry vertical, the global semiconductor fabrication material market is bifurcated into telecommunication, energy, electrical and electronics, medical and healthcare, automotive, and others. The telecommunication segment is expected to hold the largest market share over the forecast period. The expansion in the 5G networks drives the market growth.

Semiconductor Fabrication Material Market: Regional Analysis

Asia Pacific dominates the market over the projected period

The Asia Pacific is expected to dominate the global semiconductor fabrication material market. China's semiconductor industry is now among the biggest worldwide and the consumers of chips as well. For CAPEX, the Semiconductor Industry Association (SIA) estimates that the Chinese semiconductor sector invested US$12.3 billion in 2021 and US$15.3 billion in 2022, to which around 15% of the world total is attributed.

Conversely, the growing installation of new plants and the increased investments in the semiconductor sector would propel the market expansion of semiconductor production materials for Japan. To become a significant worldwide supplier of vital computer chips, the Japanese government, for instance, spent US$6.8 billion on domestic semiconductor manufacturing. Thus driving the market growth in the Asia Pacific.

Semiconductor Fabrication Material Market: Competitive Analysis

The global semiconductor fabrication material market is dominated by players like:

- JSR Corporation

- Alent Plc

- BASF SE

- Air Liquide SA

- Praxair Inc.

- Dow Chemical Company

- Air Products and Chemicals Inc.

- Kanto Chemical Co. Inc.

- Linde AG

- Taiyo Nippon Sanso

The global semiconductor fabrication material market is segmented as follows:

By Material

- Silicon Wafers

- Photomasks

- Photoresists

- Wet Chemicals

- CMP Slurry and Pads

- Gases

- Sputter Targets

- Photoresist Ancillaries

By Application

- Consumer Appliances

- Power Generation

- Electronic Components

- Others

By Industry Vertical

- Telecommunication

- Energy

- Electrical and Electronics

- Medical and Healthcare

- Automotive

- Others

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

Semiconductor fabrication materials are the raw components and elements employed in the fabrication and production of semiconductor devices, such as integrated circuits (ICs) and microchips. From wafer fabrication to device assembly and packaging, these components are vital in several phases of semiconductor processing.

The semiconductor fabrication material market is being driven by several factors such as increasing demand for semiconductors, technological advancements, growth in the automotive industry, increasing expansion of 5G networks and many others.

According to the report, the global semiconductor fabrication material market size was worth around USD 55.9 billion in 2023 and is predicted to grow to around USD 98.5 billion by 2032.

The global semiconductor fabrication material market is expected to grow at a CAGR of 6.5% during the forecast period.

The global semiconductor fabrication material market growth is expected to be driven by the Asia Pacific. It is currently the world’s highest revenue-generating market due to the increasing semiconductor industry and rising investment in innovative technology.

The global semiconductor fabrication material market is dominated by players like JSR Corporation, Alent Plc, BASF SE, Air Liquide SA, Praxair, Inc., Dow Chemical Company, Air Products and Chemicals Inc., Kanto Chemical Co., Inc., Linde AG and Taiyo Nippon Sanso among others.

The semiconductor fabrication material market report covers the geographical market along with a comprehensive competitive landscape analysis. It also includes cash flow analysis, profit ratio analysis, market basket analysis, market attractiveness analysis, sentiment analysis, PESTLE analysis, trend analysis, SWOT analysis, trade area analysis, demand & supply analysis, Porter’s five forces analysis, and value chain analysis.

Zion Market Research

Tel: +1 (302) 444-0166

USA/Canada Toll Free No.+1 (855) 465-4651

3rd Floor,

Mrunal Paradise, Opp Maharaja Hotel,

Pimple Gurav, Pune 411061,

Maharashtra, India

Phone No +91 7768 006 007, +91 7768 006 008

US OFFICE NO +1 (302) 444-0166

US/CAN TOLL FREE +1 (855) 465-4651

Email: sales@zionmarketresearch.com

We have secured system to process your transaction.

Our support available to help you 24 hours a day, five days a week.

Monday - Friday: 9AM - 6PM

Saturday - Sunday: Closed