Semiconductor Manufacturing Equipment Market Size, Share, Trends, Growth and Forecast 2034

Semiconductor Manufacturing Equipment Market By Equipment Type (Lithography Systems, Deposition Equipment, Etching Equipment, Cleaning Equipment, Inspection and Metrology Systems), By Dimension (2D ICs, 2.5D ICs, and 3D ICs), By Technology Node (Below 10nm, 10-14nm, 14-28nm, Above 28nm), By Back-End Equipment (Wafer Testing, Packaging, Dicing, Bonding, and Assembly), By Application (Logic and Memory, Foundry, Integrated Device Manufacturers), By End-User Industry (Consumer Electronics, Automotive, Telecommunications, Healthcare, Industrial), and By Region - Global and Regional Industry Overview, Market Intelligence, Comprehensive Analysis, Historical Data, and Forecasts 2025 - 2034

| Market Size in 2024 | Market Forecast in 2034 | CAGR (in %) | Base Year |

|---|---|---|---|

| USD 108.56 Billion | USD 236.55 Billion | 8.10% | 2024 |

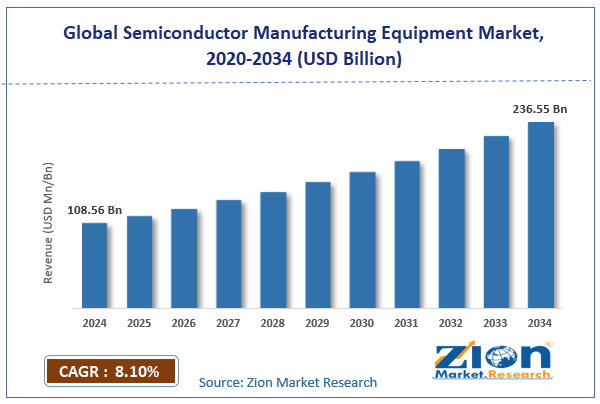

Semiconductor Manufacturing Equipment Industry Prospective:

The global semiconductor manufacturing equipment market size was valued at approximately USD 108.56 billion in 2024 and is expected to reach around USD 236.55 billion by 2034, growing at a compound annual growth rate (CAGR) of roughly 8.10% between 2025 and 2034.

Semiconductor Manufacturing Equipment Market: Overview

Semiconductor manufacturing equipment represents the specialized machinery and systems that produce integrated circuits and microchips across various technology nodes. This enables innovation, digital transformation, and advanced manufacturing across multiple industries.

The semiconductor equipment industry has transformed the global technology landscape, providing critical components for emerging technologies like AI, 5G, IoT, and advanced computing. Semiconductor equipment produces more complex and miniaturized electronic components, driving consumer electronics, automotive, telecom, and healthcare innovation.

Over the forecast period, technological advancements, demand for advanced semiconductors, complexity of chip designs, and global digital transformation will drive the market.

Key Insights:

- As per the analysis shared by our research analyst, the global semiconductor manufacturing equipment market is estimated to grow annually at a CAGR of around 8.10% over the forecast period (2025-2034)

- In terms of revenue, the global semiconductor manufacturing equipment market size was valued at around USD 108.56 billion in 2024 and is projected to reach USD 236.55 billion by 2034.

- The semiconductor manufacturing equipment market is projected to grow significantly due to increasing technological complexity, demand for advanced semiconductors, digital infrastructure expansion, investment in emerging technologies, and global digital transformation initiatives.

- Based on equipment type, lithography systems lead the market and will continue to dominate the global market.

- Based on the dimensions, 3D IC manufacturing equipment is expected to grow the most.

- Based on the technology node, equipment below 10nm is anticipated to command the largest market share by the end of the forecast period.

- Based on back-end equipment, packaging equipment is projected to lead the market.

- Based on application, logic, and memory, they are expected to lead the market during the forecast period.

- Based on end-user industries, consumer electronics will remain dominant during the forecast period.

- Based on region, Asia Pacific is projected to dominate the global market during the forecast period.

Semiconductor Manufacturing Equipment Market: Growth Drivers

Technological innovation and emerging digital technologies

In the semiconductor manufacturing equipment industry, technological innovation drives market expansion. Artificial intelligence, 5G, quantum computing, and edge computing require more advanced semiconductors.

According to recent surveys, semiconductor equipment companies have increased research and development investment to support emerging technologies.

Consumer demand for high-performance, low-power, and small-form-factor devices drives continuous technology advancement in semiconductor equipment. Automation and innovative manufacturing solutions also transform production efficiency, enabling higher precision and scalability in semiconductor fabrication.

Geopolitical strategy and technological sovereignty

Semiconductor manufacturing equipment requires a high investment and is a complex technology. Research, development, and manufacturing infrastructure costs are increasing and creating barriers to entry for new players. Advanced lithography and precision equipment are expensive and require technology expertise. Manufacturers must keep investing in the latest technologies to remain relevant in a rapidly evolving market. Public-private and cross-border collaborations are key to accelerating semiconductor innovation and production capacity.

Semiconductor Manufacturing Equipment Market: Restraints

High capital investment and technological complexity

Semiconductor manufacturing equipment requires substantial capital investment and represents a highly complex technological ecosystem. The escalating costs of research, development, and manufacturing infrastructure create significant barriers to entry for new market participants.

Advanced lithography systems and precision manufacturing equipment can cost hundreds of millions of dollars, requiring extensive financial resources and technological expertise.

Manufacturers must continuously invest in cutting-edge technologies to remain competitive in an increasingly sophisticated market. Strategic collaborations, government incentives, and industry partnerships play a crucial role in sustaining innovation and mitigating financial challenges in the sector.

Semiconductor Manufacturing Equipment Market: Opportunities

Expansion of emerging technologies and digital transformation

The growth of emerging technologies like AI, IoT, autonomous vehicles, and advanced computing systems is opening up new opportunities for the semiconductor manufacturing equipment industry. These technologies require more complex, energy-efficient, and smaller semiconductor components. Companies that can develop flexible and adaptable equipment for advanced technology nodes will have a significant market advantage.

The convergence of multiple technology domains is opening up new semiconductor manufacturing solutions. Automation and intelligent manufacturing are also key to meeting the growing demand for high-performance semiconductor devices.

Semiconductor Manufacturing Equipment Market: Challenges

Supply chain resilience and global technological competition

The semiconductor manufacturing equipment market has supply chain disruptions and global competition. Geopolitical tensions, trade restrictions, and technology export controls make manufacturing and distribution complex; different regions' technology capabilities and regulatory environments impact equipment development and deployment.

As technology becomes more strategic, manufacturers must navigate global complexity and stay ahead of the technology curve. Rising production costs and the need for continuous innovation further pressure manufacturers to optimize efficiency and invest in next-generation fabrication technologies. Increasing demand for advanced chips in AI, 5G, and automotive sectors adds further strain to the semiconductor supply chain.

Semiconductor Manufacturing Equipment Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Semiconductor Manufacturing Equipment Market |

| Market Size in 2024 | USD 108.56 Billion |

| Market Forecast in 2034 | USD 236.55 Billion |

| Growth Rate | CAGR of 8.10% |

| Number of Pages | 212 |

| Key Companies Covered | Applied Materials, ASML Holding N.V., Lam Research Corporation, KLA Corporation, Tokyo Electron Limited, SCREEN Holdings Co. Ltd., Novellus Systems Inc., Panasonic Corporation, Canon Inc., Hitachi High-Technologies Corporation, Teradyne Inc., Advantest Corporation, ULVAC Inc., Nikon Corporation, ASM International N.V. and others. |

| Segments Covered | By Product Type, By Application, By End User, By Technology, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2034 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Semiconductor Manufacturing Equipment Market: Segmentation

The global semiconductor manufacturing equipment market is segmented into equipment type, dimension, technology node, back-end equipment, application, end-user industry, and region.

Based on equipment type, the semiconductor manufacturing equipment industry is segregated into lithography systems, deposition equipment, etching equipment, cleaning equipment, and inspection and metrology systems. Lithography systems lead the market by offering critical precision manufacturing capabilities for advanced semiconductor production.

Based on dimension, the market is categorized into 2D ICs, 2.5D ICs, and 3D ICs. 3D IC manufacturing equipment is expected to grow as chipmakers increasingly adopt 3D integration for better performance, power efficiency, and miniaturization of semiconductor devices.

Based on the technology node, the semiconductor manufacturing equipment market is divided into below 10nm, 10-14nm, 14-28nm, and above 28nm. The equipment below 10nm is expected to lead the market during the forecast period, as these advanced nodes enable increasingly sophisticated and compact electronic components.

Based on back-end equipment, the market is segmented into wafer testing, packaging, dicing, bonding, and assembly. Packaging equipment will dominate the market as the industry moves toward advanced packaging solutions like 3D stacking and chiplet integration for enhanced performance and efficiency.

Based on application, the semiconductor manufacturing equipment market is categorized into logic and memory, foundry, and integrated device manufacturers. Logic and memory dominate the market due to their widespread adoption across multiple technological domains.

Based on end-user industries, the market is classified into consumer electronics, automotive, telecommunications, healthcare, and industrial sectors. Consumer electronics lead the market, driven by continuous demand for advanced, high-performance electronic devices.

Semiconductor Manufacturing Equipment Market: Regional Analysis

Asia Pacific to lead the market

Asia Pacific leads the global semiconductor manufacturing equipment market due to its robust electronics manufacturing infrastructure, technological innovation, and significant investment in semiconductor technologies. Countries like China, South Korea, Taiwan, and Japan account for a substantial portion of global semiconductor equipment manufacturing and consumption.

The region has developed comprehensive semiconductor ecosystems, supporting advanced research, manufacturing capabilities, and technological innovation. TSMC, Samsung, and Intel have a significant presence and investments in the latest manufacturing technologies in the region.

Government initiatives and funding in China and South Korea further strengthen domestic semiconductor production and reduce import dependence. Growing demand for consumer electronics, 5G, and AI applications drives investments in advanced fab technologies. Asia Pacific also has a skilled workforce and an established supply chain for large-scale semiconductor production.

As the region continues to be the leader in the global semiconductor landscape, partnerships, and technology will be key to sustaining the leadership. Focusing on sustainability and energy-efficient semiconductor manufacturing is also shaping the region's competitive edge, and companies are investing in green technologies and advanced materials to improve productivity and reduce environmental impact.

North America is set to maintain a significant market presence

North America is a key player in the semiconductor manufacturing equipment industry due to its technology leadership, research capabilities, and presence of significant semiconductor equipment companies. The U.S. is the hub of semiconductor innovation, with companies like Applied Materials, Lam Research, and KLA Corporation driving the technology.

The region has a strong venture capital ecosystem and research institutions supporting continuous semiconductor manufacturing technology innovation. Government initiatives like the CHIPS Act promote domestic semiconductor production and reduce dependence on foreign supply chains.

The growing demand for AI-driven computing, automotive chips, and next-generation communication technologies further drives investments in advanced manufacturing equipment. Collaboration between semiconductor companies, research institutions, and federal agencies makes North America a global leader in semiconductor innovation.

Recent Market Developments:

In January 2025, Applied Materials introduced advanced extreme ultraviolet (EUV) lithography systems with unprecedented precision for below 3nm technology nodes.

- In March 2025, ASML launched next-generation semiconductor manufacturing equipment featuring enhanced artificial intelligence-driven process optimization capabilities.

Semiconductor Manufacturing Equipment Market: Competitive Analysis

The global semiconductor manufacturing equipment market is led by players like Applied Materials, ASML Holding N.V., Lam Research Corporation, KLA Corporation, Tokyo Electron Limited, SCREEN Holdings Co. Ltd., Novellus Systems, Inc., Panasonic Corporation, Canon Inc., Hitachi High-Technologies Corporation, Teradyne Inc., Advantest Corporation, ULVAC Inc., Nikon Corporation, and ASM International N.V.

The global semiconductor manufacturing equipment market is segmented as follows:

By Equipment Type

- Lithography Systems

- Deposition Equipment

- Etching Equipment

- Cleaning Equipment

- Inspection

- Metrology Systems

By Dimension

- 2D ICs

- 2.5D ICs

- 3D ICs

By Technology Node

- Below 10nm

- 10-14nm

- 14-28nm

- Above 28nm

By Back-End Equipment

- Wafer Testing

- Packaging, Dicing

- Bonding

- Assembly

By Application

- Logic and Memory

- Foundry

- Integrated Device

- Manufacturers

By End-User Industry

- Consumer Electronics

- Automotive

- Telecommunications

- Healthcare

- Industrial

By Region

- North America

- The U.S.

- Canada

- Europe

- France

- The UK

- Spain

- Germany

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Table Of Content

Methodology

FrequentlyAsked Questions

Semiconductor manufacturing equipment represents the specialized machinery and systems that produce integrated circuits and microchips across various technology nodes.

The market is expected to be driven by technological innovation, increasing demand for advanced semiconductors, digital transformation initiatives, emerging technology development, and global investment in semiconductor infrastructure.

According to our study, the global semiconductor manufacturing equipment market was worth around USD 108.56 billion in 2024 and is predicted to grow to around USD 236.55 billion by 2034.

The CAGR value of the semiconductor manufacturing equipment market is expected to be around 8.10% during 2025-2034.

The global semiconductor manufacturing equipment market will register the highest growth in Asia Pacific during the forecast period.

Key players in the semiconductor manufacturing equipment market include Applied Materials, ASML Holding N.V., Lam Research Corporation, KLA Corporation, Tokyo Electron Limited, SCREEN Holdings Co. Ltd., Novellus Systems, Inc., Panasonic Corporation, Canon Inc., Hitachi High-Technologies Corporation, Teradyne Inc., Advantest Corporation, ULVAC Inc., Nikon Corporation, and ASM International N.V.

The report comprehensively analyses the global semiconductor manufacturing equipment market, including an in-depth discussion of market drivers, restraints, emerging trends, regional dynamics, and future growth opportunities. It also examines competitive dynamics, technological innovations, the evolving landscape of semiconductor manufacturing technologies, industry requirements, and strategic developments shaping the global semiconductor equipment ecosystem.

Zion Market Research

Tel: +1 (302) 444-0166

USA/Canada Toll Free No.+1 (855) 465-4651

3rd Floor,

Mrunal Paradise, Opp Maharaja Hotel,

Pimple Gurav, Pune 411061,

Maharashtra, India

Phone No +91 7768 006 007, +91 7768 006 008

US OFFICE NO +1 (302) 444-0166

US/CAN TOLL FREE +1 (855) 465-4651

Email: sales@zionmarketresearch.com

We have secured system to process your transaction.

Our support available to help you 24 hours a day, five days a week.

Monday - Friday: 9AM - 6PM

Saturday - Sunday: Closed